Bank woes raise questions about the Fed’s next move.

Investors’ sudden hunger for U.S. government bonds has pushed yields to their lowest levels in months—and created much uncertainty about what happens next in the Fed’s battle against inflation.

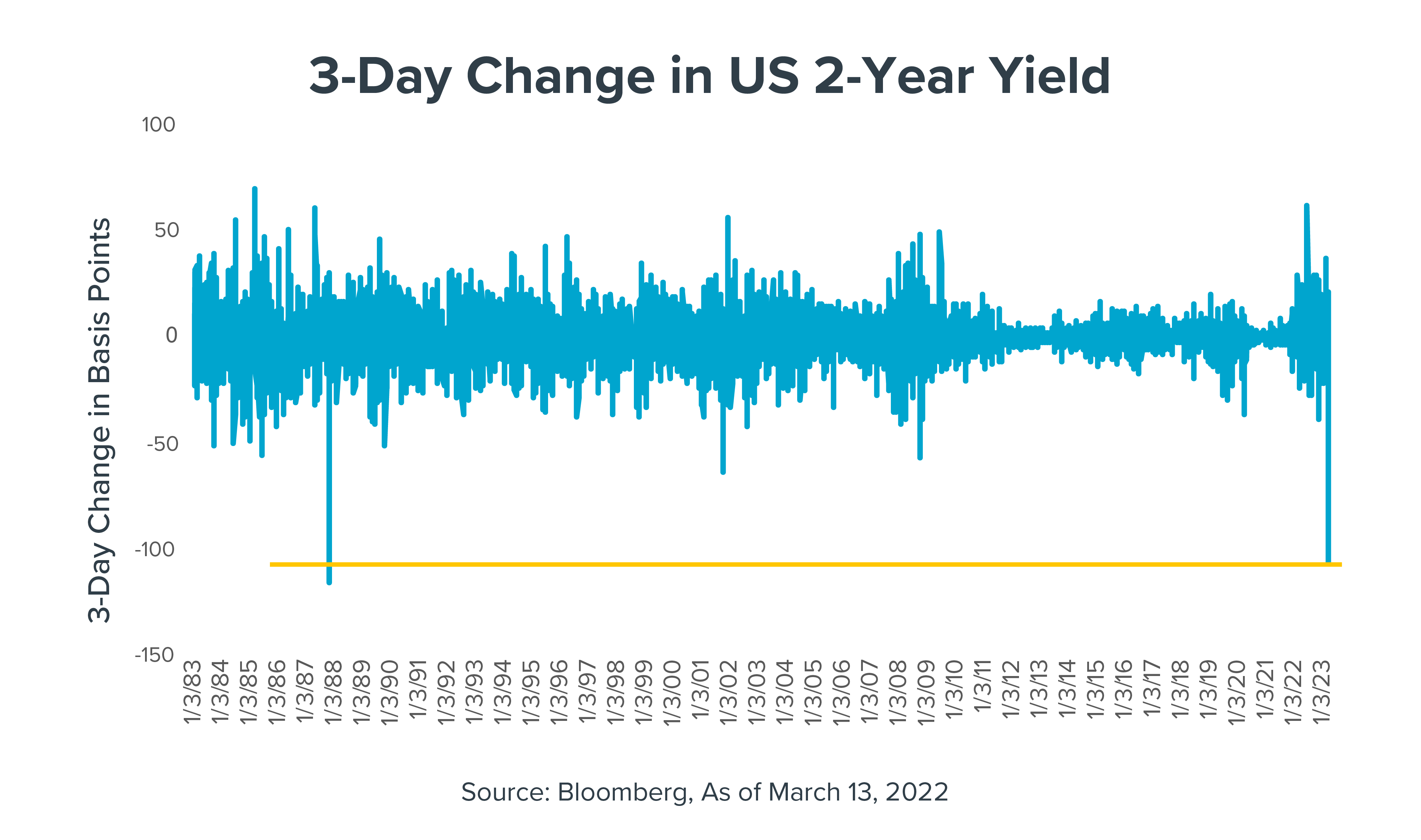

In a notable move, the yield on the 2-year Treasury plummeted 106 basis points from last Wednesday’s close through Monday’s close—the second largest three-day decline in the T-note’s yield over the last 40 years (see the chart). The 2-year Treasury yield now sits at its lowest level of the year.

Yields went into freefall as investors, fearful that fallout from Silicon Valley Bank’s collapse last week could spread throughout the banking sector, raised doubts that the Fed will continue with its current pace of interest rate hikes when it meets later this month. Until this recent financial shock, investors largely agreed the Fed would raise rates in March by at least 25 basis points in its continued efforts to stamp out high inflation. Now, some on Wall Street think the Fed will hit pause as it assesses the impact of recent events–or even reverse course.

Example: Last week, it was estimated that the Fed would raise rates four times between late December 2022 and the end of 2023. As of Monday’s close—just a few days later—the market was expecting the Fed to cut interest rates three times by year-end.*

Concerns about the financial system’s health also drove investors to scoop up high-quality government bonds, putting further downward pressure on those bonds’ yields (as bond yields decline when bond prices rise.)

The upshot: We’re in murkier waters than we were just a little more than a month ago. Back then, we noted that the financial markets were predicting lower volatility in the 2-year Treasury yield going forward. That’s not the case today. And if the yield on an essentially risk-free asset like a short-term Treasury note ends up fluctuating wildly, it becomes virtually impossible to accurately value equities with any degree of confidence.

New data to be released before the next Fed meeting may offer some clarity about the direction of rates. For now, however, we believe the extreme sentiment shifts we’re seeing in the wake of the Silicon Valley Bank failure mean it’s likely a good time to exercise caution.

*Federal Funds rate estimated using Bloomberg’s World Interest Rate Probabilities (WIPR). WIRP is a statistical function developed by Bloomberg that uses fed funds futures and options to infer the implied probability of future FOMC decisions.

This commentary is written by Horizon Investments’ asset management team. Past performance is not indicative of future results. Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry, or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice, or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments.

The investments recommended by Horizon Investments are not guaranteed. There can be economic times when all investments are unfavorable and depreciate in value. Clients may lose money.

Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns. All investing involves risk of loss, and in periods of market growth, risk mitigation strategies can be expected to lag in performance behind equity strategies that do not focus on risk mitigation.

This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent. Forward-looking statements cannot be guaranteed.

Reference to an index does not imply that any account will achieve returns, volatility, or other results similar to that index. An index’s composition may not reflect how a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, restrictions, sectors, correlations, concentrations, volatility or tracking error targets, all of which are subject to change. Individuals cannot invest directly in any index.

Other disclosure information is available at www.horizoninvestments.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2023 Horizon Investments LLC