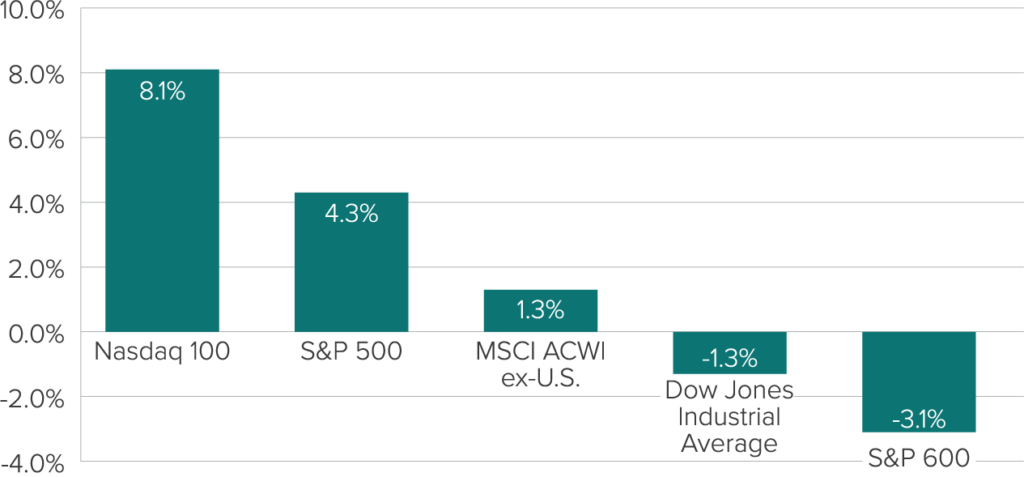

Overall, stocks delivered another quarter of strong gains during the three-month period ending June 28, 2024. For the quarter:

- The Nasdaq 100 returned 8.1%.

- The S&P 500 index returned 4.3%.

- Foreign shares also rose, with the MSCI ACWI ex-U.S. index of developed and emerging international markets up 1.3%.

Two exceptions: The Dow Jones Industrial Average was down 1.3%, while the S&P 600 index of small-company stocks fell 3.1%.

Exhibit 1: Major Stock Market Indices Returns (Q2 2024)

We are focused on a few themes and trends that we believe will be particularly important going into the third quarter of 2024:

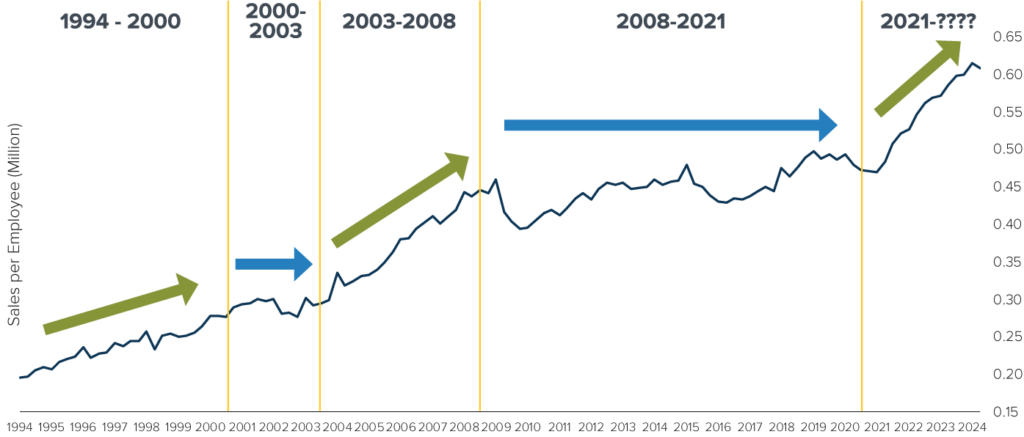

1. Artificial Intelligence (AI) May Drive the Next Productivity Boom

AI technology’s explosive growth has boosted tech stocks (does Nvidia ring a bell?) to massive valuations. Despite the attention AI tech companies are receiving, the most exciting aspect of this technology is its potential to impact businesses in virtually all industries—and, in doing so, influence the broader economy.

Let’s consider when Internet- and web-based technologies were emerging in the mid-1990s. As that tech went from being simply “tech cool” to “business cool,” it helped companies across a variety of sectors significantly improve their operations through enhanced capabilities within information technology systems (see Exhibit 2).

Exhibit 2: Thirty Years of Worker Productivity

Today, a growing number of companies across industries are recognizing how emerging AI technology tools have the potential to streamline many aspects of their businesses. As this awareness grows, AI could help fuel the next phase of increased worker productivity – potentially resulting in higher corporate profits for numerous sectors and stronger overall economic growth. Indeed, as Exhibit 2 shows, we’ve already seen a spike in average revenue per employee recently. AI may be instrumental in taking it even higher.

2. Consumers Are in Great Shape (No, Really!)

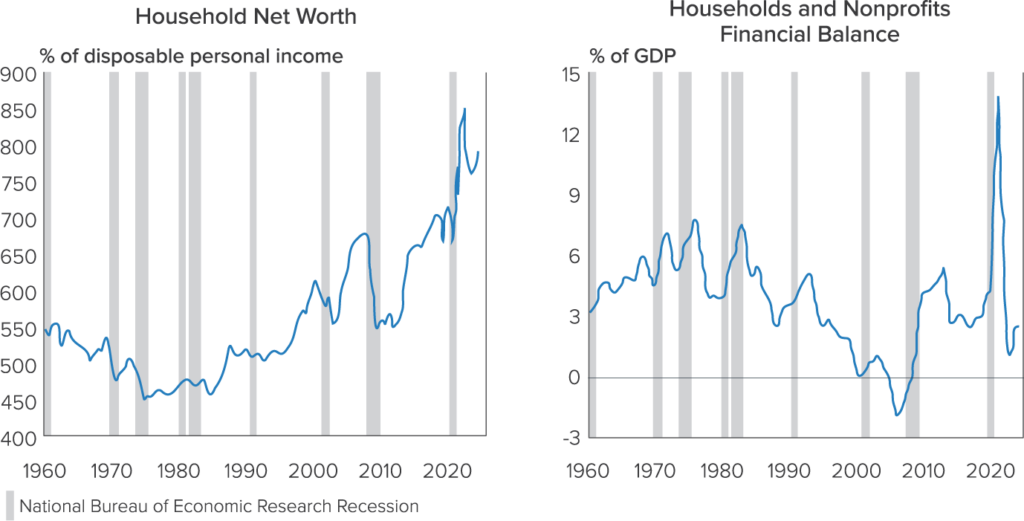

Many surveys evaluating consumer sentiment have indicated a general sense of pessimism among consumers despite the resilience of the economy and the job market. For example, although total debt has hit record levels, consumers’ ability to service that debt—to comfortably make their principal and interest payments—appears to remain strong and well under control.

We can draw this conclusion because American consumers—whose spending accounts for two-thirds of U.S. economic growth—remain in robust financial shape. Consider two facts:

- Household net worth today is at a near-record high, while household debt is significantly lower than it has been for much of the past 70-plus years (see Exhibit 3).

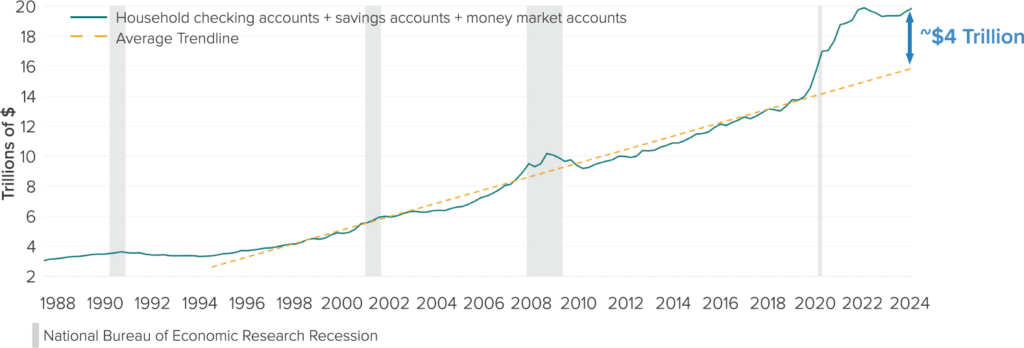

- Consumers are flush with cash. As seen in Exhibit 4, current balances in consumers’ checking/savings/money market accounts total approximately $20 trillion—roughly $4 trillion more than the long-term trend suggests those balances should be.

The upshot: Consumers still have tremendous amounts of money to put to work in the economy and the financial markets.

Exhibit 3: Household Net Worth is Large; Household Debt is Small

Exhibit 4: Consumer Balances in Checking/Savings/Money Market Accounts

However, this begs the obvious question: Given their objectively strong financial position, why do consumers seem so down in the dumps?

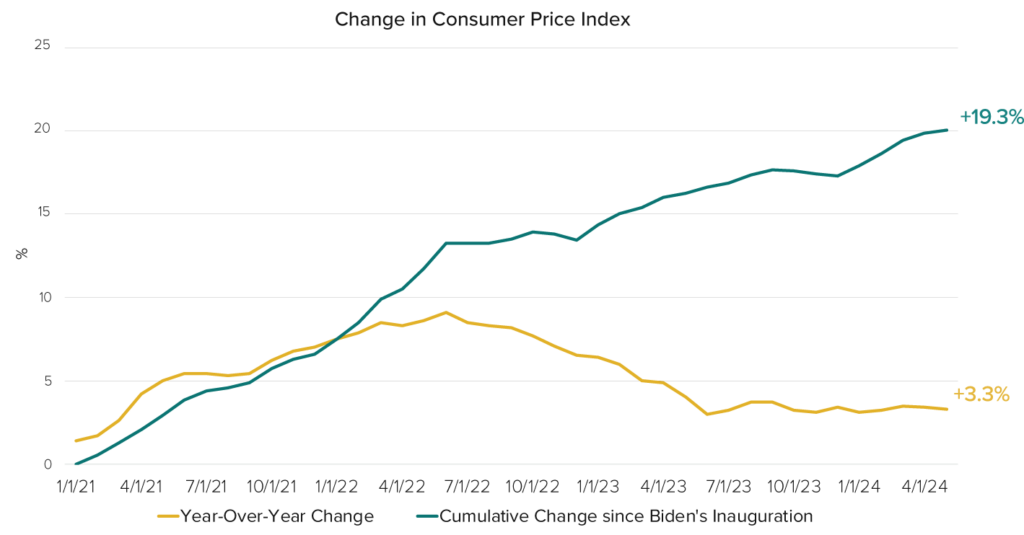

One likely answer can be seen in Exhibit 5, which shows how inflation is being viewed in two very different ways:

- In the eyes of economists, investors, and the media, inflation has been moderating for some time now. As the yellow line shows, the year-over-year rise in the Consumer Price Index was just 3.3% in May—close to its long-term average and much lower than the 9.1% reading in mid-2022.

- The general public, however, is focused on the green line in the chart below. When they buy groceries or go out to dinner, they notice that prices are still nearly 20% higher than they were a few years ago. Even if they can easily absorb those higher costs, they’re disheartened by what they see.

Exhibit 5: Inflation – “Good” or “Bad” Depends on Who You Ask

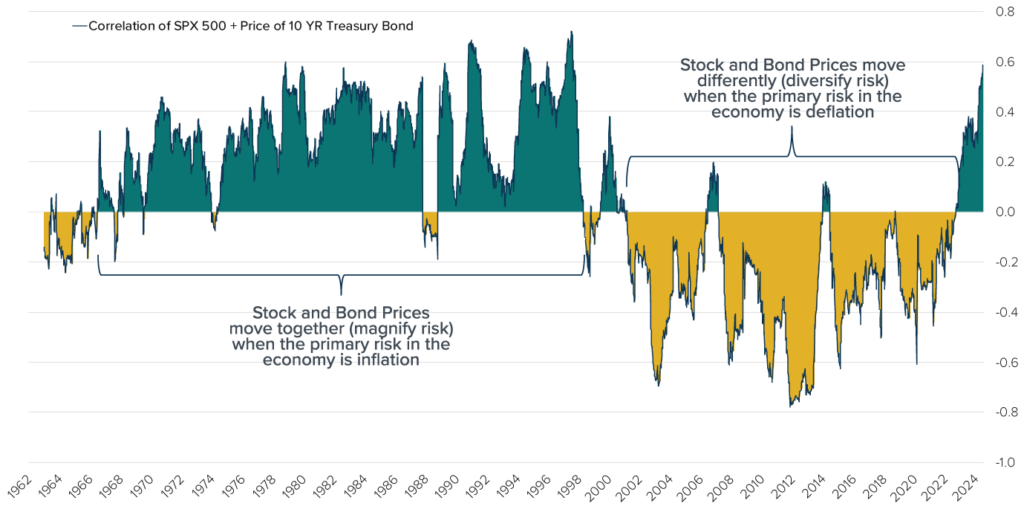

3. It’s a Good Time to Rethink Portfolio Risk Management

The traditional role of bonds for many investors—an asset class for reducing overall portfolio volatility—is shifting in today’s market, necessitating an evolving approach to risk management.

That’s because (as seen in Exhibit 6) stocks and bonds typically enjoy their lowest correlation with each other in environments where inflation is low and the primary risk to the economy is deflation—such as the roughly 20-year period through 2022. During such times, bonds tend to “zig” when stocks “zag,” and vice versa.

Unfortunately, fixed income tends to be less useful as a portfolio diversification/risk reduction tool in an environment like today’s. When the primary economic characteristic is inflation, stock and bond prices tend to become increasingly positively correlated—moving together, as was generally the case from the mid-1960s through the late 1990s rather than apart (see Exhibit 6).

Exhibit 6: Correlation of Stocks and Bonds, Inflationary Versus Deflationary Environments