OVERVIEW

Following a third-quarter slump, stocks roared back to life during the final three months of 2023.

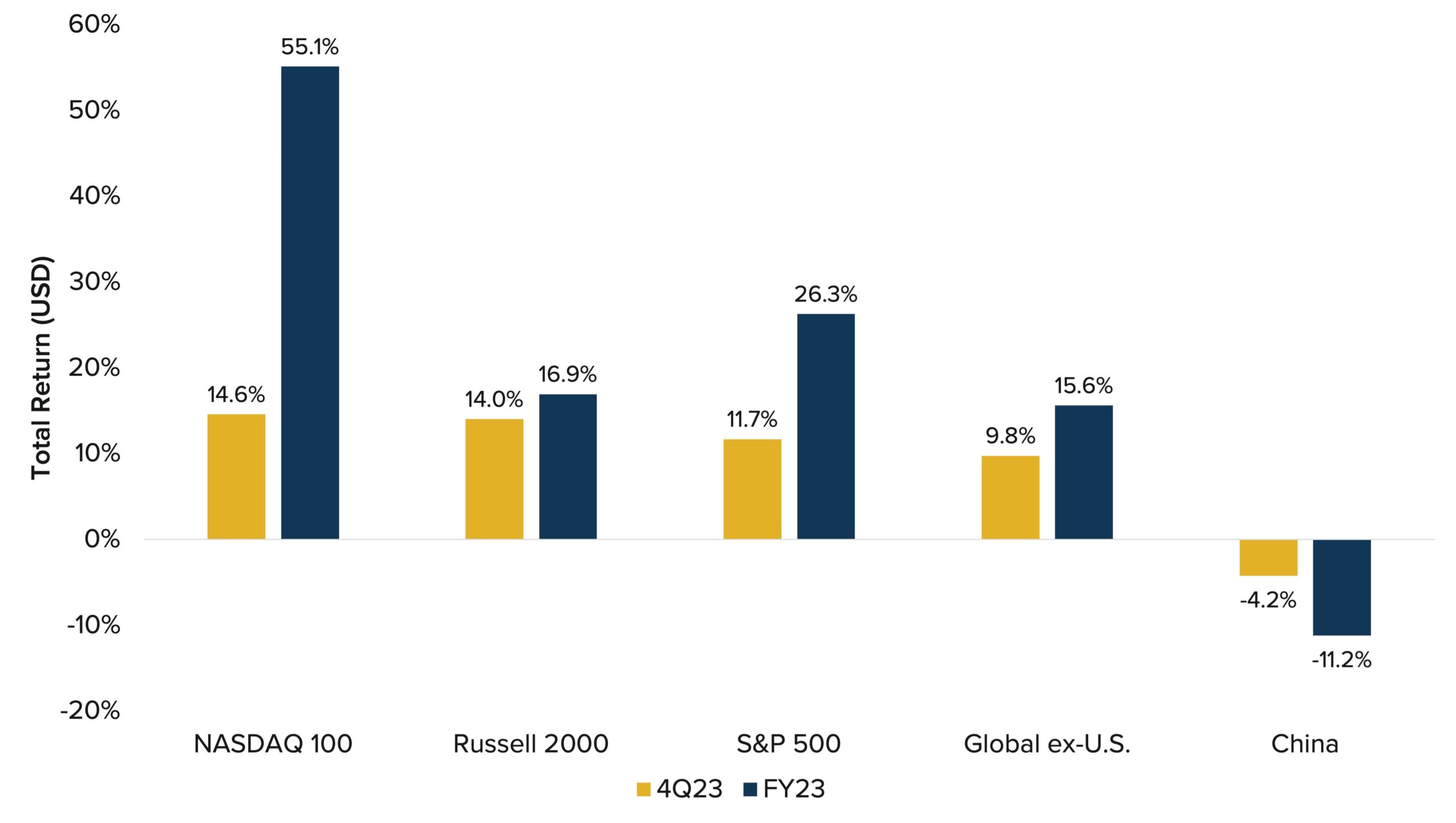

- The S&P 500 index of large-company stocks rallied 11.7% during the fourth quarter, including a 4.4% rise in December, and ended the year just shy of a new all-time high.

- According to Dow Jones Market Data, the index’s rise in the final three months of 2023 marked its biggest quarterly percentage jump since the fourth quarter of 2020.

- The small-cap Russell 2000 index also delivered its best quarterly return since the fourth quarter of 2020, up 14% (gaining 12.2% in December alone).

Fourth-quarter gains were primarily driven by increased investor confidence that the Federal Reserve Board was finished with its campaign of raising interest rates to combat inflation—and that the Fed might even begin cutting interest rates in the coming months. Continued strength in the job market and robust consumer spending also fueled strong economic growth and corporate profits that helped push stock prices higher.

Major equity market indices also delivered strong gains for the year. The Nasdaq 100 led the way, soaring 55.1% in 2023 due largely to investor enthusiasm over developments in artificial intelligence (AI) technology. In fact, a handful of tech stocks (the so-called “Magnificent 7”) were largely responsible for the market’s returns in 2023. Meanwhile, the S&P 500 was up 26.3% for the calendar year, the Russell 2000 gained 16.9%, and the Dow Jones Industrial Average rose 16.2%.

Exhibit 1: Major Stock Market Indices Returns (4Q2023 and Full-Year 2023)

Source: Bloomberg, as of 12/29/2023

International equities also gained ground, overall, but lagged behind shares of U.S. stocks— with the MSCI ACWI ex-U.S. index of developed and emerging international markets returning 9.8% for the quarter. Foreign shares were weighed down largely because of weaker-than-expected growth in China, where the MSCI China index fell 4.2% last quarter. Additionally, growth prospects in Europe remained relatively weak compared to those in the U.S.

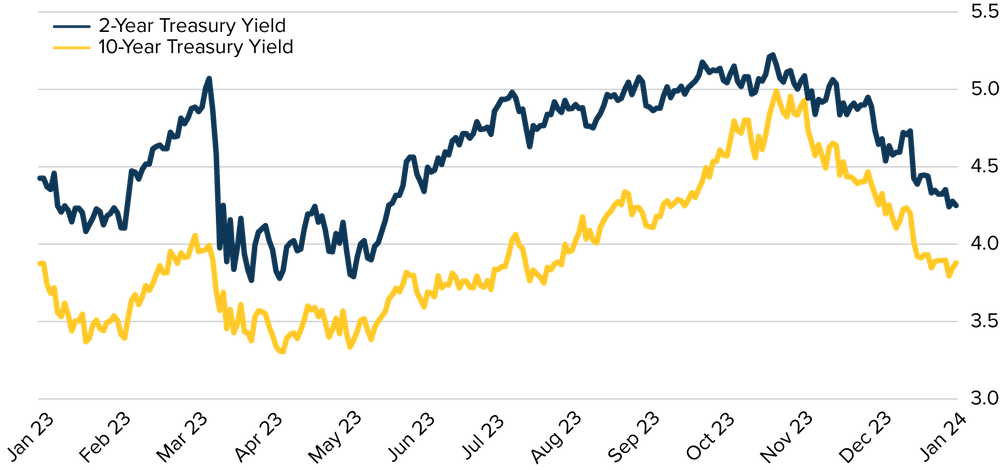

The fixed-income markets experienced significant volatility throughout the year, including during the fourth quarter (see Exhibit 2). The yield on the 10-year Treasury spiked early in 2023 due to a more resilient economic outlook, then plummeted as fears around regional banks spread in March. After official actions to stem the contagion, the 10-year yield marched steadily higher to reach levels in October that were last seen in 2007. The yield then fell sharply, amazingly finishing the year nearly where it began. That year-end fall occurred in the wake of the Fed appearing to be done with its campaign of inflation-fighting interest rate hikes.

Meanwhile, as seen in Exhibit 2, the policy-sensitive 2-year Treasury yield followed a similar pattern—starting the year at 4.43% and falling at 3.75% in March, then topping out in October before ending 2023. For the full year, the 2-year yield ended about 20 basis points lower than it began despite 100 basis points of hikes by the Fed in 2023.

Exhibit 2: Yield on the 10-Year Treasury, 2023

Source: Bloomberg, as of 12/29/23

NOT YOUR PARENTS’ BUSINESS CYCLE

2023 began with a chorus of voices predicting an imminent, unavoidable recession. The year ended not just without a recession occurring but with a growing number of investors, analysts, strategists, and even Main Street Americans calling for the much-hoped-for “soft landing”—an economy and job market growing at just the right speed to be sustainable coupled with a low, stable inflation rate.

At Horizon, we never shared the belief that a recession in 2023 was a foregone conclusion. To the contrary, throughout the year we highlighted the many aspects of economic strength that we believed could enable the economy to avoid an extended period of negative growth.

Many investors have struggled to recognize these positive economic factors—and they wonder how the overall mood in the market has veered from doom and gloom to general optimism. To paraphrase David Byrne, lead singer of the Talking Heads: “How did we get here?”

One key is recognizing that the economic conditions we’ve seen since the pandemic began in 2020 are largely unlike any most investors have ever experienced. The upshot: This isn’t your parents’ business cycle.

Some key factors that are making today’s business cycle behave in unexpected ways include the following:

- High deficit spending levels. Despite low unemployment, spending by the federal government relative to the revenues taken in by the government remains at levels often seen during economic downturns. That means rather than supporting a weak economy— which is often the goal behind strong deficit spending—the current level of government outlays is helping fuel additional growth in an economic environment that’s already reasonably healthy.

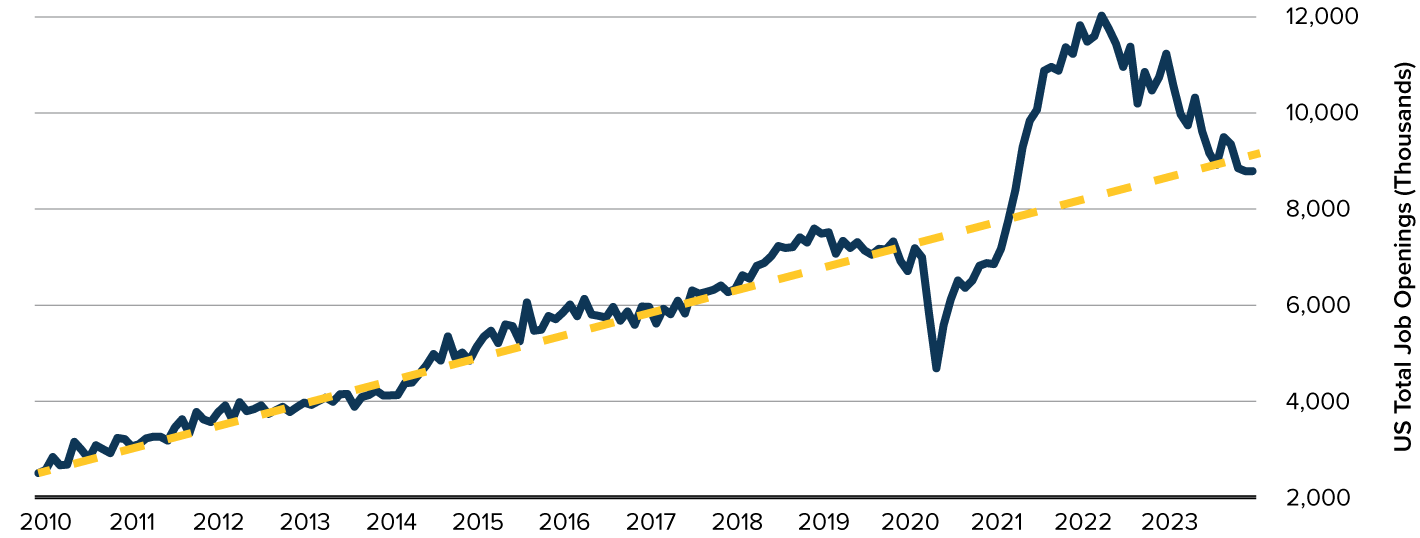

- A wild ride for jobs. The number of job openings plummeted during the pandemic, then soared higher during 2021 and into 2022 (see Exhibit 3). This extreme differential between the low point (too few job openings) and the high point (too many job openings) is unprecedented in recent times. That volatility prevented the labor market from functioning effectively—which, in turn, made it challenging to accurately assess the state of the job market at various points. Note, however, that job openings have now fallen back toward their more normalized pre-pandemic levels. Clearly, the labor market has softened this year—but that’s from a significantly abnormal peak. What’s more, it’s difficult to characterize this current labor market as weak given the long-term trend (the yellow dots in Exhibit 3).

Exhibit 3: Labor Market Is Softening – But It’s Not Soft

Source: Bloomberg, as of 12/29/23

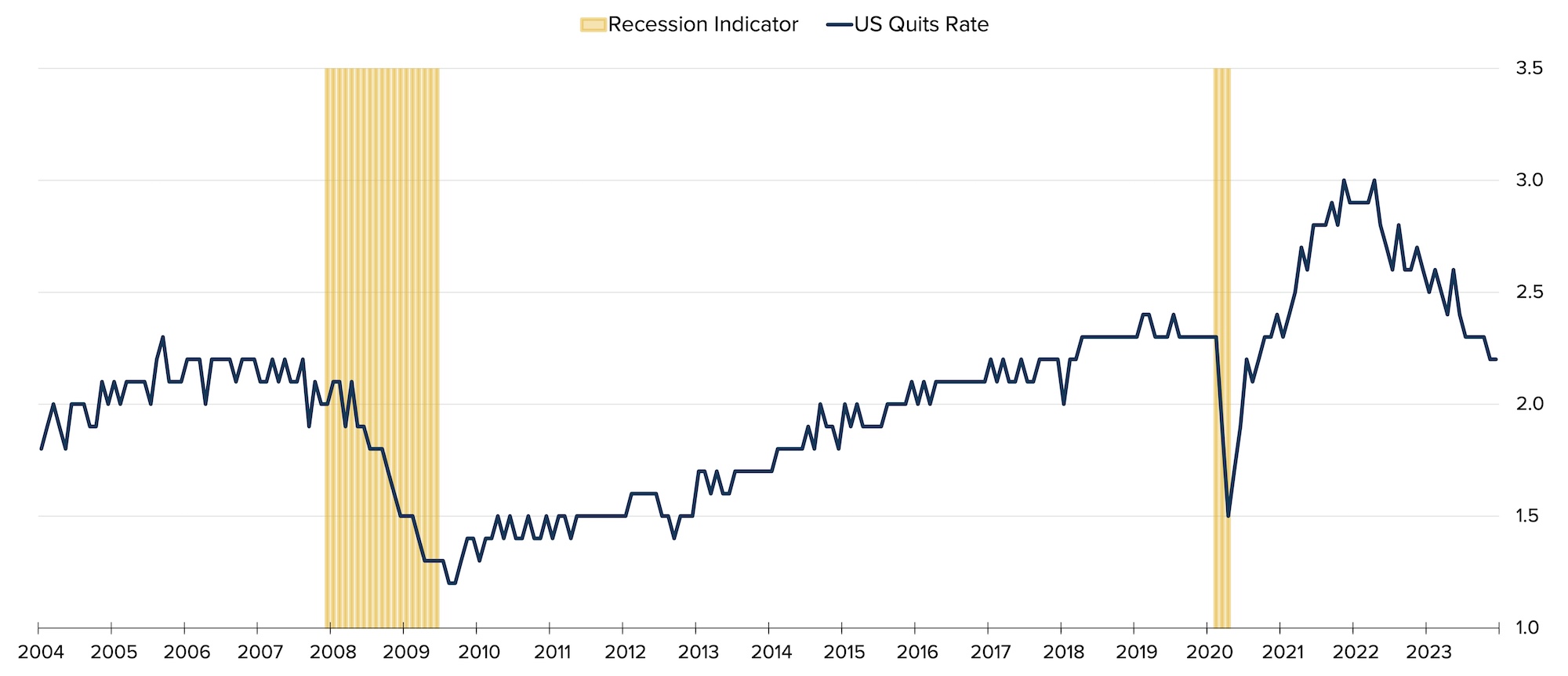

Likewise, the so-called “quit rates” (essentially a measure of labor market tightness – people are willing to quit their jobs if they have another lined up or if they know for sure they can get one) experienced a similar divergence from the pandemic low point versus the post-pandemic peak, as seen in Exhibit 4. That dynamic looks nothing like it would in a typical business cycle—nor does it even look like it did during the Great Recession of 2008-2009, in which the steep decline was followed by a much slower recovery. But the quit rate today also seems to now be finding its natural level again, as supply and demand in the job market regains balance. That, in turn, should further help wage pressures to abate.

Exhibit 4: Job Openings Returning to Pre-Pandemic Level

Source: Bloomberg, as of 12/29/23

Ultimately, as long as people are working, we think it’s tough to make a case for an impending recession. Consider one of the most reliable recession indicators—the so-called Sahm Rule, which says a recession begins when the national unemployment rate’s three-month moving average rises by 0.5 percentage points or more from its low during the previous 12 months. As Exhibit 5 shows, the Sahm Rule is nowhere near being triggered at the moment.

Exhibit 5: The “Sahm Rule” Recession Indicator Is Nowhere Near Signaling a Recession

Source: Bloomberg, as of 12/29/23

Disjointed spending patterns. Consumers’ spending habits and patterns have truly flip-flopped in recent years in ways that are unlike those seen in other business cycles. During the pandemic, spending on goods soared as people bought products to use at home—while spending on services that involved going out plummeted. The reversal started in 2022, with goods-based buying seeing a major slowdown and service sectors experiencing a significant spending jolt. In 2023, for example, the Transportation Security Administration screened the most airline passengers ever in a single day—nearly 3 million on June 30th alone, compared to just 100,000 in the early days of the pandemic.

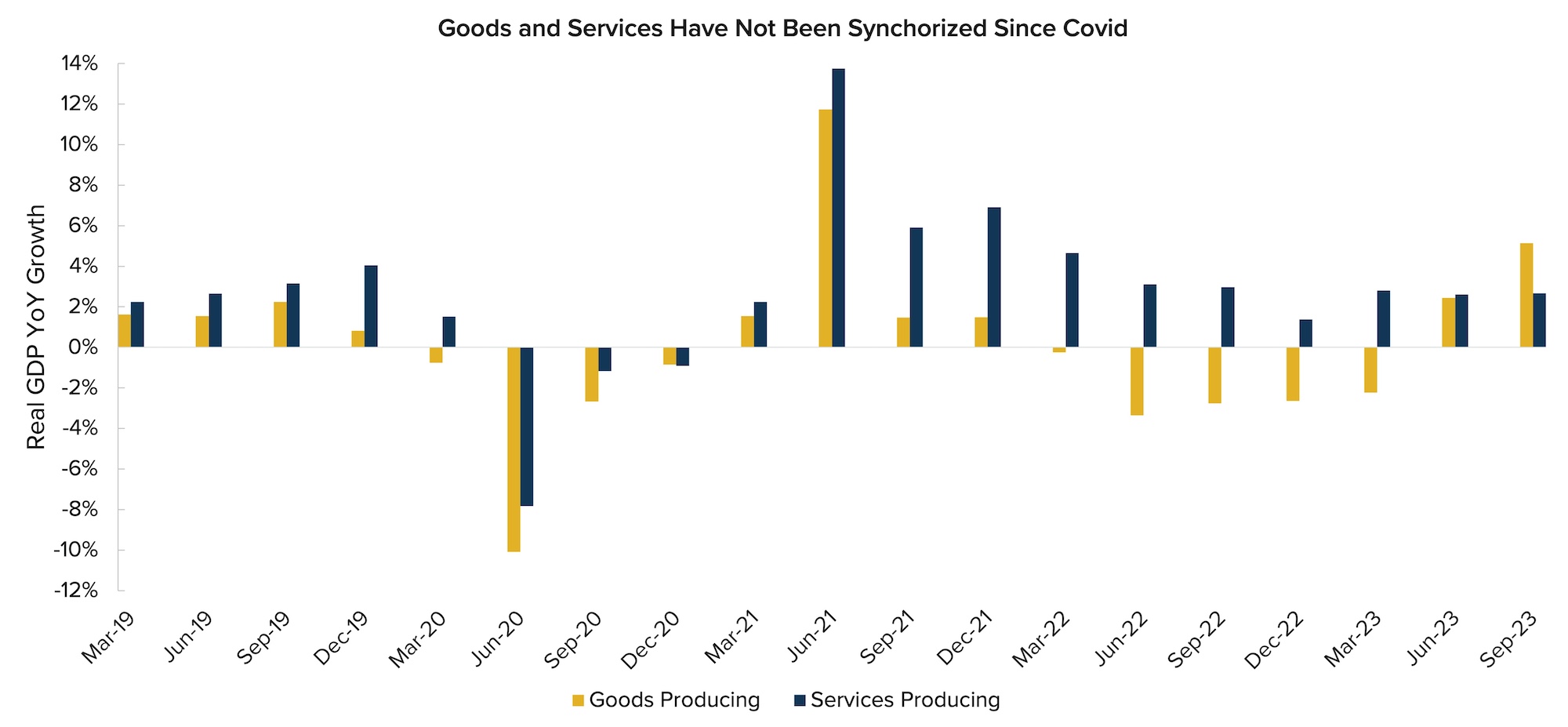

Waves of economic weakness. In typical economic cycles, such as in 2019, supply and demand across many areas of the economy often move in lockstep (see Exhibit 6). But due to the disjointed spending patterns noted above, that hasn’t always been the case since the pandemic. In some ways, that’s been beneficial: Rather than broad-based weakness across the majority of the economy, we’ve experienced more of a see-saw effect—with periods where manufacturing has been up sharply while services have been weak, and then vice versa. Note, as seen in Exhibit 6, that goods-producing GDP contracted in 2022 and into 2023 while services-producing GDP was on the rise. This dynamic may have helped the overall economy avoid recession. Note, too, that more recently, goods and services have begun to resemble their more traditional pattern.

Exhibit 6: Manufacturing Slumping While Services Expanding

Source: Bloomberg, as of 12/29/23

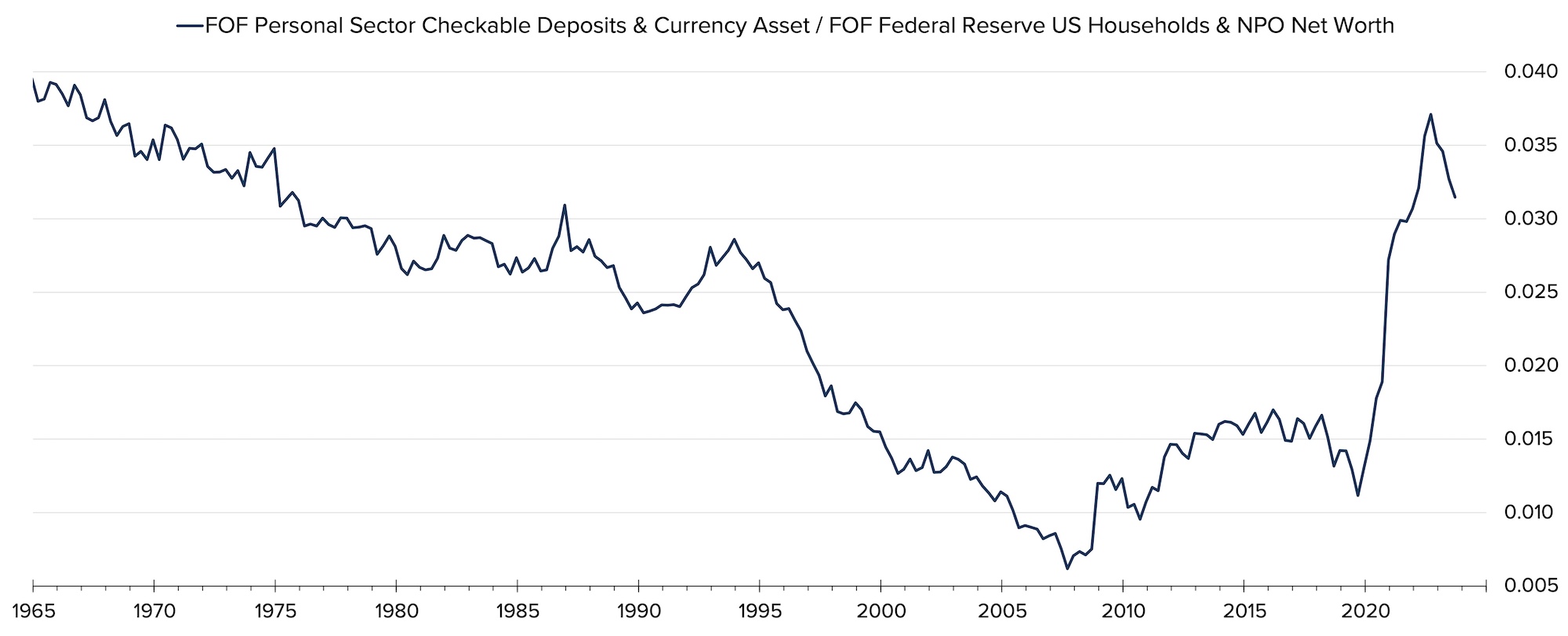

A surprisingly resilient consumer. In traditional business cycles, consumers overspend and over-borrow. They deplete their savings and end up far too leveraged, and these excesses ultimately contribute to an economic downturn. Currently, however, the consumer remains quite resilient. As seen in Exhibit 7, for example, deposit levels in personal checking accounts are higher than they’ve been in decades (despite having fallen in recent months).

Exhibit 7: Consumers’ Checking Account Balances Are High

Source: Bloomberg, as of 12/29/23

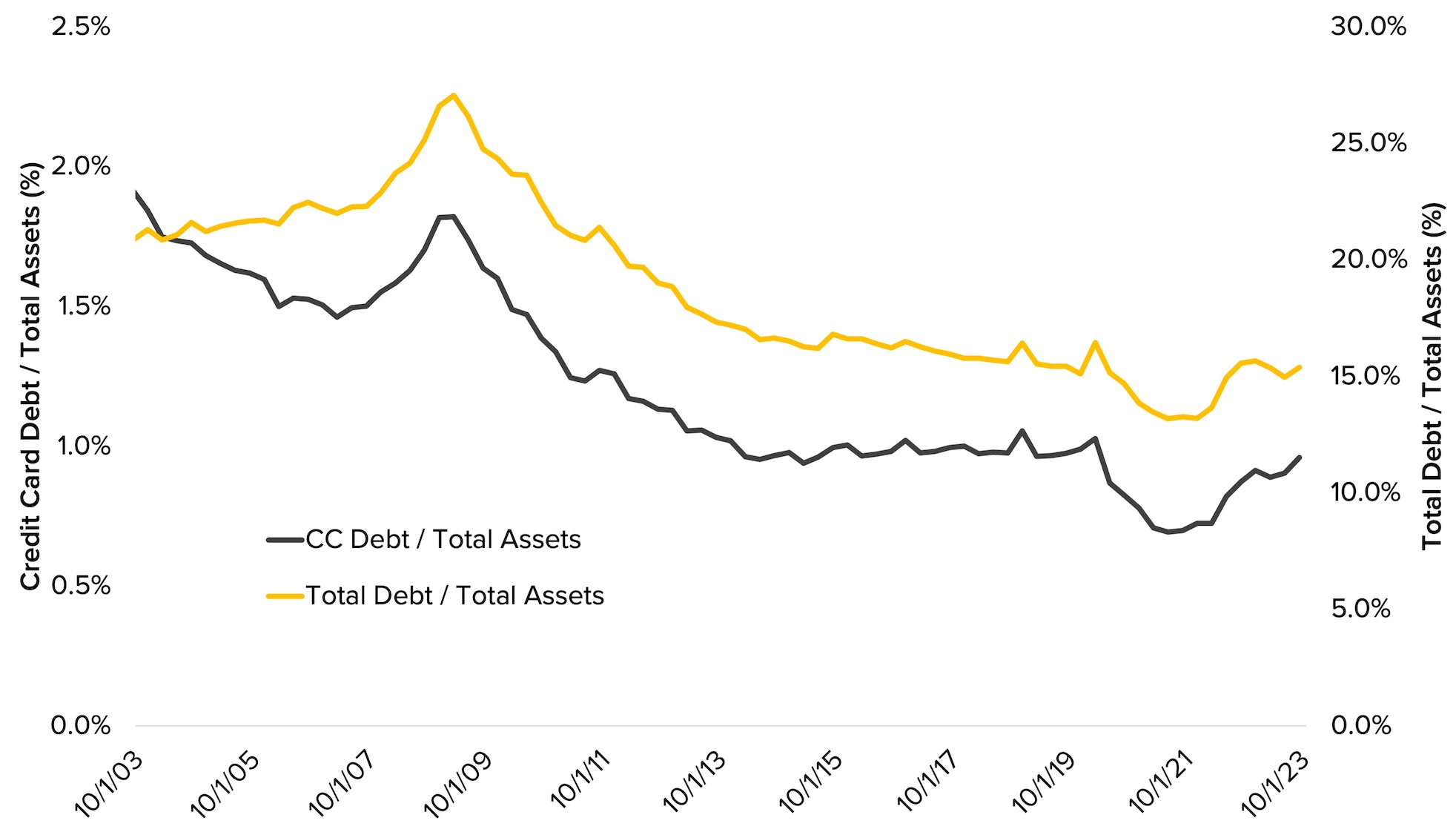

On the flip side, overall household leverage has actually fallen since 2019. This is true of credit card debt and total debt (see Exhibit 8).

Exhibit 8: Household Debt as a % of Total Assets

Source: Bloomberg, as of 12/29/23

Despite media headlines of a “credit card debt crisis,” Americans’ overall financial health remains strong enough to absorb and manage that debt. For example:

- Just 0.3% of bank-issued credit card holders were delinquent for 60 to 89 days. That’s the same percentage it was in late 2019, shortly before the pandemic began—and it’s far lower than the 1.2% in early 2010 and the 1.5% in early 1997.

- The same dynamic is true of retail-issued credit card holders: 0.9% today versus 0.9% in late 2019, 1.6% in early 2010, and 1.8% in early 1997.

Yet another narrative—high interest rates hurting homeowners’ financial health—has also been greatly exaggerated. Mortgage rates have risen along with overall interest rates, of course. But that’s not causing pain for most existing homeowners with a mortgage: The effective mortgage rate of around 3.8% remains low. Higher rates also aren’t hurting the financial health of the 40% of homeowners today who don’t have a mortgage at all.

NEW MARKET HIGHS: JUMP IN OR RUN AWAY?

Investors during the past 12 months have gravitated toward cash, driven by the near-constant calls for an imminent recession that would crush stock prices and by the high (by recent standards) interest rates available on that cash due to the Fed’s monetary policy.

Of course, that recession didn’t materialize—and while investors in cash earned around 5% on average, the S&P 500 marched toward an annual return of 26.3%. As noted above, that index ended 2023 close to its all-time high. Likewise, bonds outperformed cash-equivalent assets for the year (with nearly all the gains in bonds occurring during the final six weeks of 2023).

In the wake of the stock market’s returns this year, many investors may now find themselves uncertain about what to do next:

- Investors who avoided or underweighted equities in 2023 may worry that they have missed out on the gains to be had—and that buying when the market is so close to its all-time high carries too much downside risk.

- Investors who were significantly invested in stocks this year and benefited from the gains may share a similar fear—that maintaining or raising their equity allocation now could expose them to big losses, and perhaps they should “take their profits” instead.

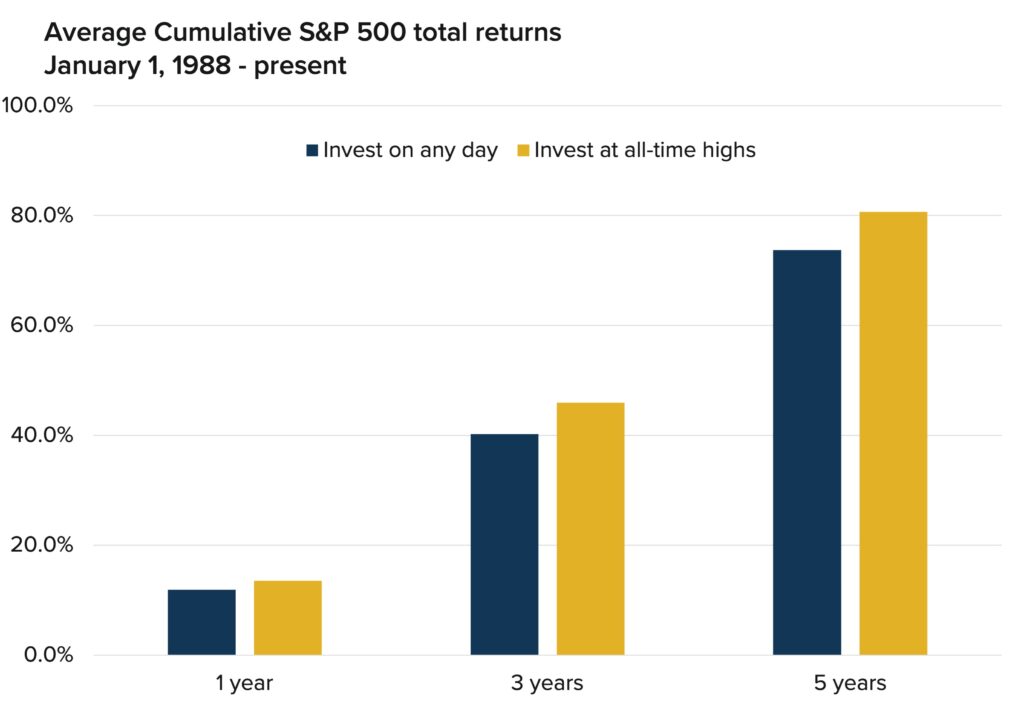

The future cannot be predicted with certainty, of course. However, a look at past occurrences when markets hit new highs may offer some important insights for investors wondering whether now is the time to buy into stocks—or run away from them.

Consider the return of investors who buy only on days when there is a market high versus those who buy on any random day. Exhibit 9 shows that investing when the market hits a high has worked out well historically.

Exhibit 9: Investing At New Market Highs

Source: Bloomberg, calculations by Horizon Investments, as of 12/29/23

New highs don’t necessarily indicate the market has peaked and is due for a fall—in much the same way that a big decline or new low doesn’t automatically mean the market has hit bottom.

Indeed, consider just how often the stock market hits new highs, as seen in Exhibit 10.

Exhibit 10: S&P 500 Number of New All-Time Highs (By Decade)

Source: Bloomberg, as of 12/29/23

But what accounts for stocks’ continued strong performance, generally, after hitting new highs? We think one likely factor could be increased market participation and better investor sentiment. Our behavioral biases typically cause us to put our money on current winners. This was evidenced as recently as December when the world’s largest ETF (the SPDR S&P 500) attracted more than $20 billion in a single day—the largest single-day flow for any ETF in history. As more investors flock to stocks, new assets can help push prices even higher.

This dynamic could be especially powerful in the coming year. The reason: Investors currently hold a tremendous amount of money in cash—around $6 trillion as of early December. Even a moderate percentage of that cash getting reallocated to equities could help push stocks higher.

There’s an additional reason why investors nervously holding on to cash may want to consider re-deploying some of that money into equities. It’s the same one that drove so many investors to cash in the first place: The Federal Reserve Board’s interest rate policy. The Fed has likely finished raising interest rates for the foreseeable future—and may soon start cutting rates to help fuel the economy.

Should that occur, the money held in cash and short-term instruments will start earning less— perhaps far less, since their yields are highly dependent on what the Fed does. In contrast, the prospects for stocks are likely to be better:

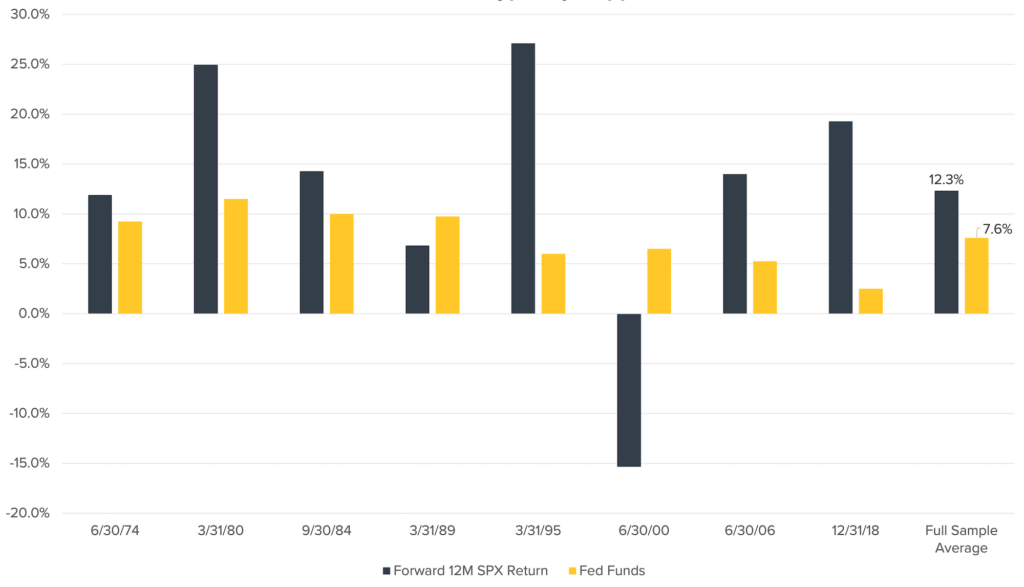

Looking at the last eight conclusions to Fed tightening cycles going back to 1970, the S&P 500’s forward 12-month return was positive in seven of those eight periods (see Exhibit 11).

The stock market’s returns have historically been robust once rates top out, with the S&P 500 gaining 12.3% on average during the 12 months after the Fed stopped raising rates. The average peak federal funds rate—which influences the interest rates on CDs and other “risk-free” financial instruments—over that period was just 7.6%.

The stock market’s 12-month return exceeded the peak federal funds rate 75% of the time after the Fed stopped raising rates.

Exhibit 11: History Shows Strong Stock Returns After Rates Peak

Source: Bloomberg, as of 12/29/23

For goals-based investors, the mental comfort and sense of safety that cash can provide may be far outweighed by the strength of stock market returns in a stable or falling rate environment.

Ultimately, new highs in the stock market shouldn’t cause you to assume the worst is about to happen. New highs occur frequently. And while some of them obviously are the peaks that presage a major decline, most result in more new highs—and additional gains for investors.

LOOKING AHEAD

We believe several aspects of the economy and the financial markets look encouraging as we begin 2024. For example:

- The labor market, though slowing, remains robust.

- Consumers continue to look strong and we remain unconcerned about current levels of consumer debt or credit card balances.

- Inflation continues to trend downward, potentially giving the Fed more latitude to cut interest rates.

- Debt issued by corporations looks manageable, particularly if rates start to come down and companies can issue new debt at lower levels.

- Many year-over-year financial comparisons may look extreme, but it’s important to remember that such comparisons involve historically distorted levels.

Other developments give us pause, such as:

- Growth outside of the U.S. is a concern, given the relatively weak prospects for both China and Europe.

- Downbeat consumer sentiment, if it stays at recent low levels, could prompt people to rein in their spending.

- Bond market volatility remains relatively high, making it more difficult to value equities and other assets with confidence.

- A reacceleration in the housing market and other interest rate-sensitive sectors could catch the Fed off guard, leading to “higher for longer than expected” interest rates.

On balance, we expect stocks to once again outperform fixed-income—and both of those asset classes to outperform cash and cash equivalents—in 2024, for several reasons:

- As inflation continues to fall, the market expects the Fed to cut interest rates in 2024 by perhaps six times. Additionally, more global central banks overall now anticipate cutting rates than they do raising them. As noted above, central bank rate cuts tend to boost equity prices.

- Worker productivity is on the rise. As AI and similar productivity-enhancing technologies are more fully implemented, productivity should continue to strengthen—helping to boost growth without fueling higher inflation, raise real living standards, and benefit asset prices.

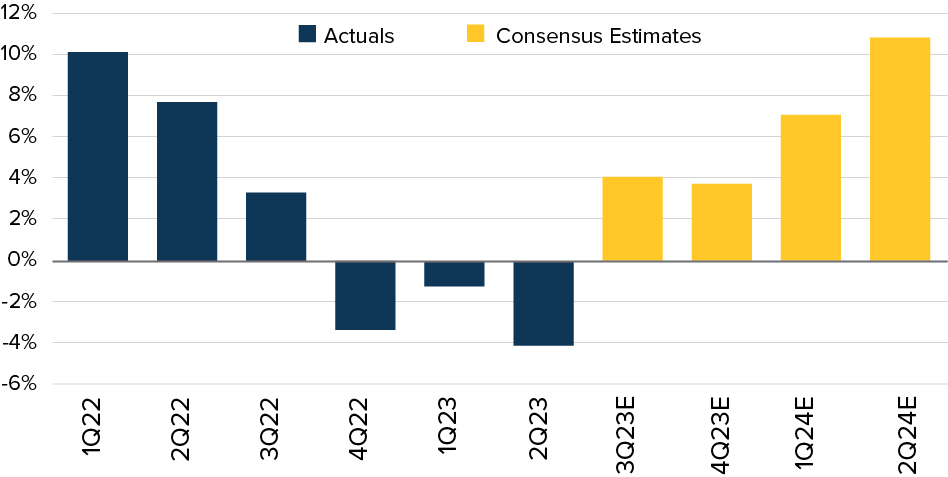

- The earnings recession appears to be over, with year-over-year estimates now firmly back in positive territory (see Exhibit 12).

Exhibit 12: The Earnings Recession Is Likely Over

Source: Bloomberg, as of 12/29/23

These developments may favor certain market segments more than others. We will be looking at company projections this coming earnings season to assess how management teams are viewing their overall businesses and how they are integrating AI and other technologies into their daily operations.

As always, we will continue to monitor for emerging opportunities. Given the atypical dynamics of the current business cycle, as noted above, there are strong possibilities that market prices will become disconnected in ways that may offer opportunities. Consider, for example, the surprising small-company stock rally in December that took small-caps 12% higher for the month. Similar tactical opportunities may develop in the coming months.