The Federal Reserve’s decision this week to hurry up and end its bond-buying by the end of Q1 next year has come none too soon as rising inflation begins to be cemented in the public’s mind.[1]

A consistent concern of the Fed is that consumers’ inflation expectations could become ‘’unanchored.’’ Meaning that the roughly 2% annual inflation pace that the central bank shoots for would be rejected by Americans for a larger number. That potentially higher number would come with the risk of causing a so-called wage-price spiral. That’s when workers demand more pay to compensate for the higher cost of living, and that, in turn pushes up the cost of goods and services, which sparks further competitive rounds of pay raises and price hikes.

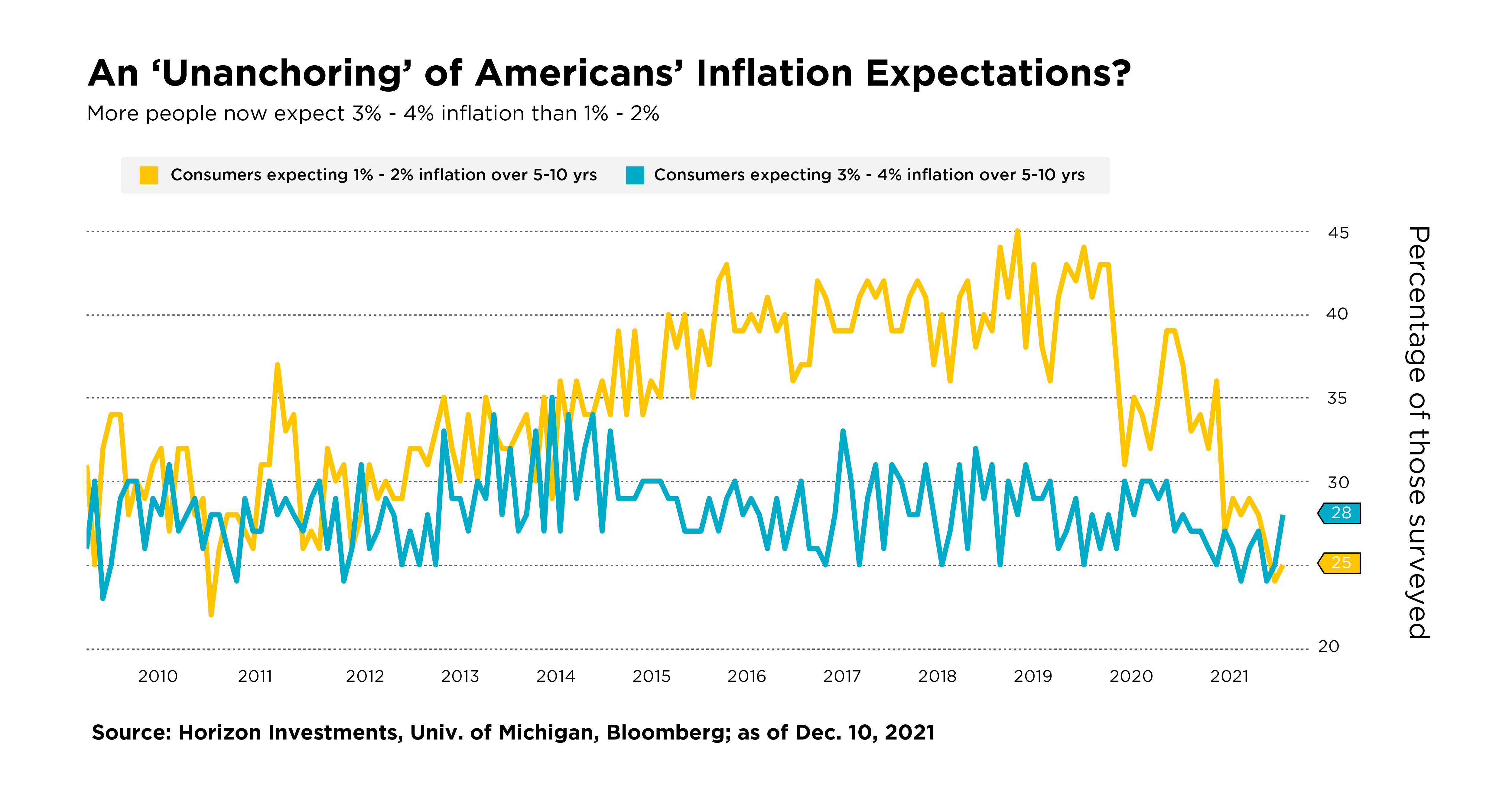

‘’Unanchored’’ might be developing. The University of Michigan’s most recent monthly consumer sentiment survey found that 28% of respondents see an inflation rate of 3% to 4% over the next five to 10 years. They now outnumber the 1% to 2% group, which had dominated for many years.[2]

University of Michigan survey director Richard Curtin said consumer confidence among low-income households surged this month, and was based on expectations of rising wages. That, he said, ‘’suggests an emerging wage-price spiral that could propel inflation higher in the years ahead.’’[3]

We think that has to be nipped in the bud by the Fed. Because letting it spiral out of control would likely force the Fed to aggressively raise interest rates, essentially squashing inflation by causing a recession. For the time being, we think that worst-case scenario has a low probability of happening. That’s due, in part, to the Fed’s tapering decision and its new forecast to possibly raise interest rates three times in 2022.

The Federal Reserve’s high-wire act that balances moving fast enough to quell inflation, but not so fast that a recession unfolds, isn’t guaranteed to succeed. Stocks and bond traders will probably vacillate between hope and fear for many more months as the Fed navigates these unusual circumstances.

Goals-based investors may want to consider preparing for potentially bigger swings in the value of their portfolios in 2022 as the inflation-versus-interest-rates debate plays out. While surveys such as the one from the University of Michigan suggest the macroeconomic background could be changing, it could be some time before anyone can say for certain that it is.

Investors who believe high inflation and rising interest rates pose a threat to their goals may want to think about enlisting the help of their advisor to make a list of portfolio changes they’d consider making to address those risks.

If preserving accumulated wealth has now become the primary investment goal, then Horizon Investments would say an investor is in the Protect stage of their investment journey. A strategy, such as Horizon’s Risk Assist®, may be able to help them navigate this uniquely demanding period that requires a balance between preserving wealth and continuing to grow assets to reach their financial goals.

Related Articles:

Read Our 2022 Outlook: The Next `Unprecedented Year

Inflation Sticker Shock Is Spreading to More Everyday Products

If Inflation Returns, Bond’s Diversification Power May Disappear

Essentially Nothing. That’s How Much Bonds May Return Over Next Five Years