It’s one thing for the Federal Reserve to set interest rates at essentially zero during an emergency. But to promise to keep them there for years to come is potentially setting up the next wave of Baby Boomer retirees to be crushed by zero.

The Fed’s zero interest rate policy (ZIRP) is scrambling the traditional maxim that a retiree’s portfolio should rest mainly on fixed-income assets. But it’s not just bonds that are yielding a pittance. Other saving vehicles, such as certificates of deposit, may not be a good replacement as their interest rates are likely too tiny to generate the income people need. Those Baby Boomers who haven’t retired yet (only about half of them have) and their advisors are wrestling with a question that has a complex answer: how do you replace fixed income in the age of ZIRP?

“I’m much more worried about falling short of a complete recovery and losing people’s careers and lives that they built because they don’t get back to work. I’m more concerned about that than about the possibility, which exists, of higher inflation.”

– Fed Chairman Powell, Jan 27, 2021 FOMC Press Conference

Cash Trashed

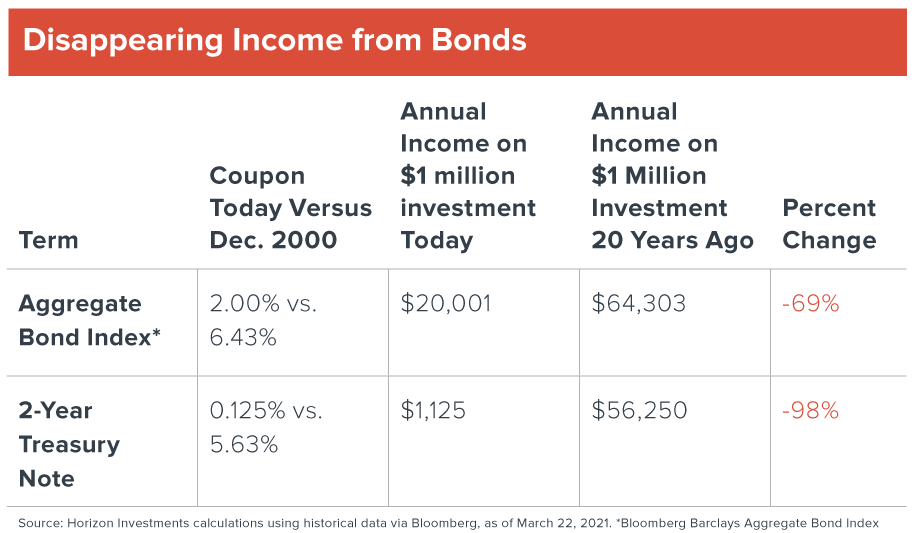

Twenty years ago, when the first wave of Baby Boomers were in their 50s and getting serious about retirement planning, bonds would have seemed like a safe and effective place to park their stock market gains to fund their golden years. For example, one million dollars invested twenty years ago in a broad fixed-income investment, as represented by the Bloomberg Barclays Aggregate Bond Index, would have produced annual, pre-tax income of about $64,000, according to Horizon Investments’ calculations.

Today the same one-million dollar investment generates just $20,000 in annual income. That’s a 69% drop. It’s far worse in the short-end of the bond market. The income from a million dollars invested in two-year Treasury notes has plunged 98% over the last two decades to about $1,125 today!

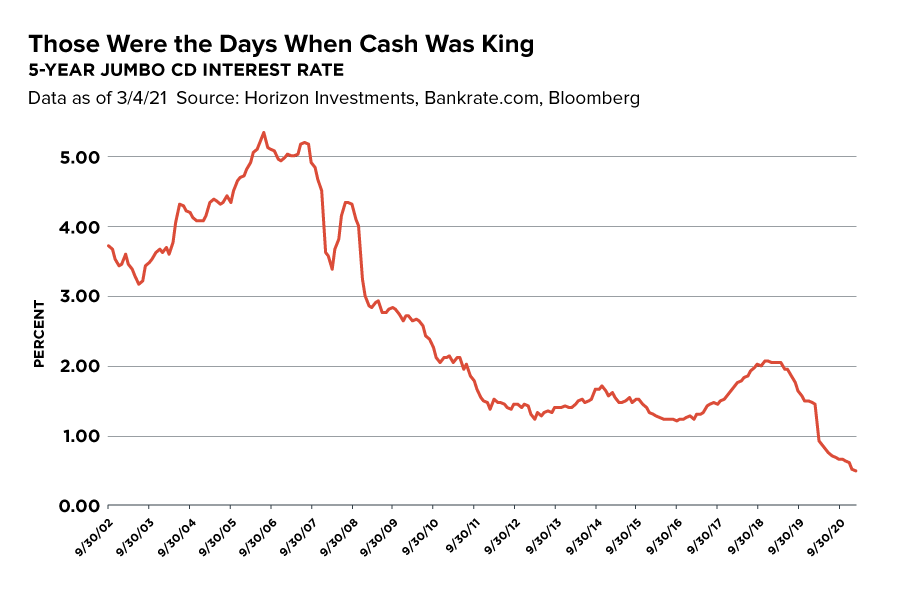

And if you were a retiree who wanted to take as little financial market risk as possible, there was always the option of jumbo certificates of deposit. In the mid-2000s, returns on cash were sometimes over 5%. Today, jumbo CDs pay about 0.5%, or $5,000 a year, pre-tax, on a million-dollar deposit.

Low Yields Are Just the Beginning

Painful as the hit to income is from the drop in yields, there are other problems with bonds that are being caused by ZIRP.

The opening weeks of 2021 have been a case study of what can go wrong with buying bonds at today’s low yields. The Bloomberg Barclays Aggregate Bond Index is down 3% year to date on a total return basis through the end of March, and volatility has shot up. That raises the specter that bonds will likely be a source of portfolio volatility rather than acting as a damper.

A more insidious issue is that losses on the fixed-income part of a portfolio can quickly snowball because of how low yields are at the start of a selloff. Even a seemingly small move in yields can have large consequences.

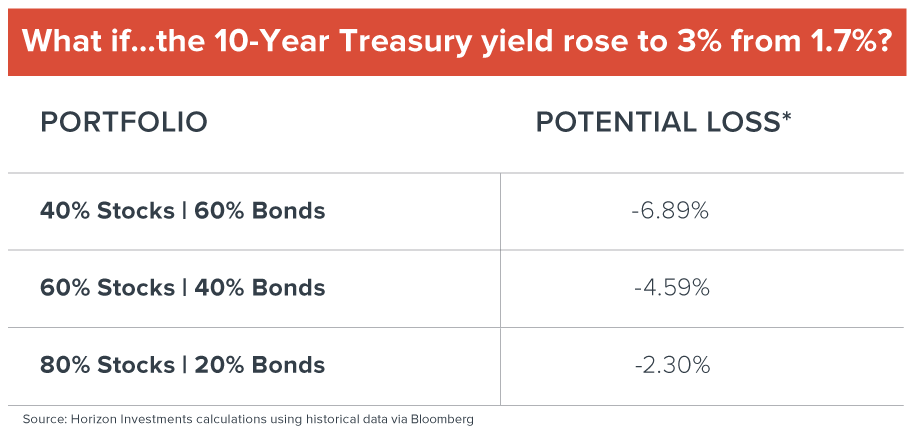

A 40/60 equity and bond portfolio might suffer a loss of 6.9% if the 10-year yield were to jump to 3%, according to Horizon Investments’ calculations. To put that potential loss in context, it would be larger than the 5.4% retreat suffered in March 2020 for Bloomberg’s generic 40% equities/60% bonds portfolio.2

Another often-cited reason to own bonds is to provide diversification when stocks fall, but that also is in doubt. If the equity market drops, yet inflation expectations continue to rise, investors may shun bonds generally, but especially those that mature in two to five years when the corrosive effects of inflation play a much bigger role.

Inflation isn’t an issue just for the so-called belly of the Treasury market. At the 10-year mark, the current yield is too small to offset the expected increase in the cost of living a decade from now. The inflation-adjusted yield – or real yield – of the 10-year is a negative 0.7%.

“Fixed-income investors worldwide – whether pension funds, insurance companies or retirees – face a bleak future.”

– Warren Buffett’s letter to Berkshire Hathaway shareholders, Feb 27, 20211

When Life Gives You Lemons…

Now that we see the potential problems associated with fixed-income investments, what would be an appropriate response? The “right” answer is going to be different in each situation amid a growing list of choices, some more complex than others. Financial advisors can help people sort through the options. Advisors can also serve as educators, teaching people how the alternatives work and their unique benefits and downsides.

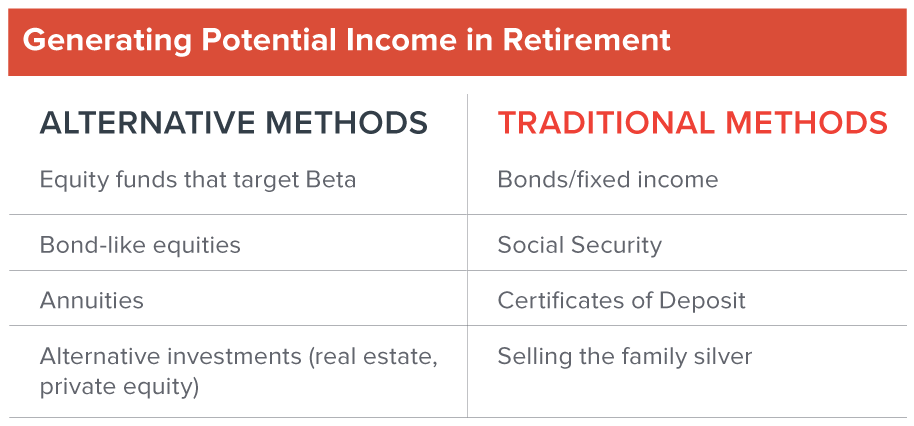

A fixed-income alternative that’s growing in popularity – because it’s easy to understand and explain – is an 80/20 equity and bond portfolio. Dubbed the “new 60/40,” this portfolio partially alleviates potential bond problems by simply cutting exposure. And a bigger tilt to stocks offers the potential for higher investment gains, which are needed if someone is planning for a long retirement. For goals-based financial plans, it’s plain to see that there’s little sense in letting 40% of a portfolio potentially do nothing in the age of ZIRP. Horizon Investments believes advisors should consider using some form of hedged equity for an 80/20 portfolio that’s being used to reduce fixed-income exposure.

Reducing bonds does carry benefits. Returning to our example above on what the effect would be if the 10-year yield rose to 3%, an 80/20 mix would lose 2.3% versus a loss of 4.6% for a 60/40 portfolio, according to Horizon Investments’ calculations.

Another alternative method for retirement income is to build a portfolio that captures a portion of a stock index’s return – what’s known as targeting Beta. Such a portfolio aims to have less volatility than its benchmark, yet it can also take part in the long-term growth of capital that’s been historically true of stock market investing. For example, a portfolio with a Beta target of 0.5 means only half of the return of a stock market index is captured.

Goals-Based Investing Is About Tradeoffs

Other bond alternatives are more complex, yet they fit Horizon Investments’ view that goals-based planning centers on choosing among tradeoffs in the pursuit of a goal, rather than chasing performance. Advisors should be prepared to discuss how the investment allocation choices they’re considering fit into a person’s risk tolerance and behavioral profile.

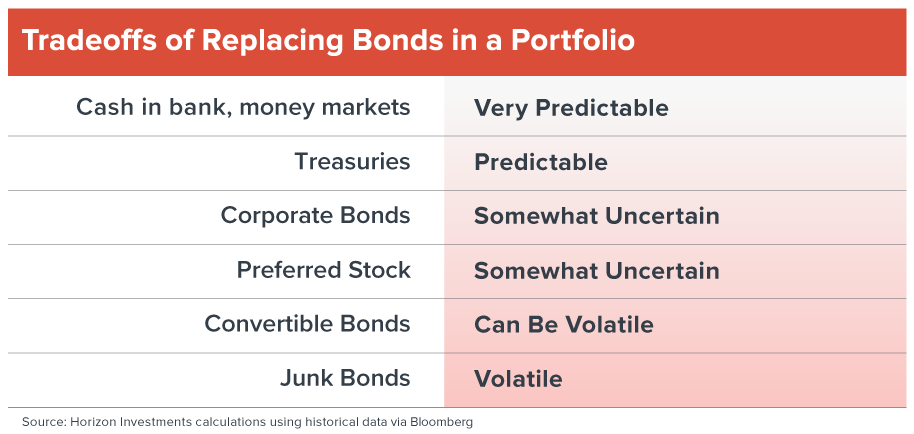

High-yield bonds – or junk bonds – can generate large returns in bull markets, and they typically carry higher yields than can be found in Treasuries and investment grade bonds. With the potential reward, though, comes higher investment risk. And high-yield bonds historically have produced levels of volatility that are similar to stocks.

Preferred stock and convertible bonds are considered bond-like from both a performance and yield point of view, though they go further out the risk spectrum compared to Treasuries. The potential downside is that both are subject to the changing financial health of the company issuing the securities. Returns can also shift based on the interest rate landscape and the performance of the stock market.

Annuities are growing in popularity with advisors given their potential for higher yields compared to Treasuries, possible protection against principal loss and the benefit of adding stability to a portfolio that’s invested in more volatile assets, such as equities. Also gaining more attention are alternative asset classes that are becoming democratized, such as buying shares of art masterpieces or investing in real estate.

The Times They Are a-Changin’

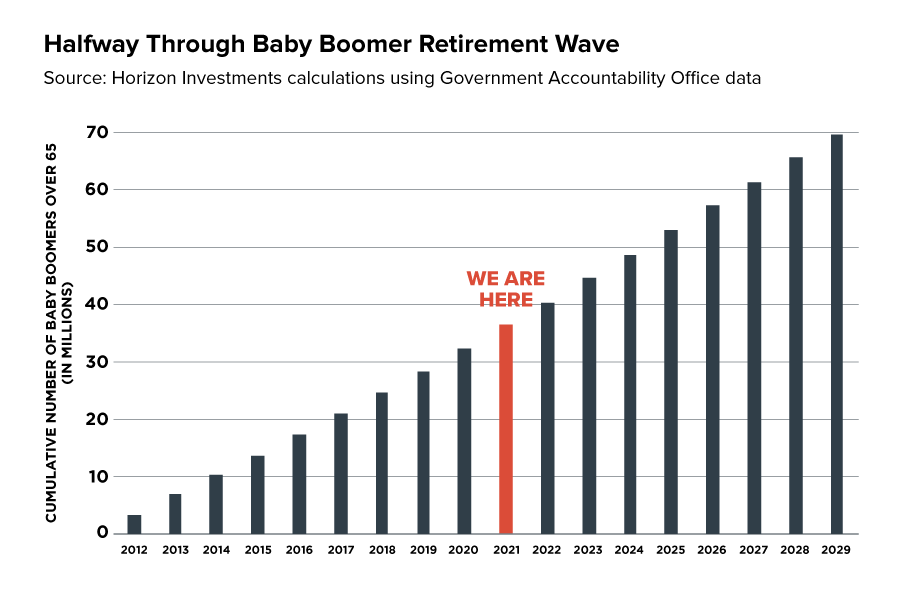

The multi-decade bull market in bonds seems like it has run out of steam. And some market pundits say they believe a bear market is now unfolding. Horizon Investments’ view is that getting caught up in the debate over whether or not there is a bear market in bonds is a mistake for advisors and their clients, considering only half of Baby Boomers are over 65 years old. We think it’s better for their retirement planning to prepare for years of low interest rates, a phenomenon that’s already entrenched in the U.S. Consider that the 1.7% yield on the 10-year Treasury note was first reached in the autumn of 2011!

In our view, the stretch of low rates will continue so long as the Federal Reserve keeps ZIRP in place. And Chairman Powell is promising that will be the case for at least the next few years. As the stretch of time with low rates gets longer, there will likely be more bond-market alternative investments rolled out. That means financial advisors should be prepared to navigate the pluses and minuses of those products and give clients advice on how best to integrate them into a goals-based financial plan.

1https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20210127.pdf

2The generic 40/60 portfolio consists of a 40% allocation to the Bloomberg Large-Cap index and a 60% allocation to the Bloomberg Barclays U.S. Aggregate Bond index