Inflation Sticker Shock Is Spreading to More Everyday Products

It’s not your imagination. Month after month, the prices of more and more goods and services are going up at a shockingly fast rate.

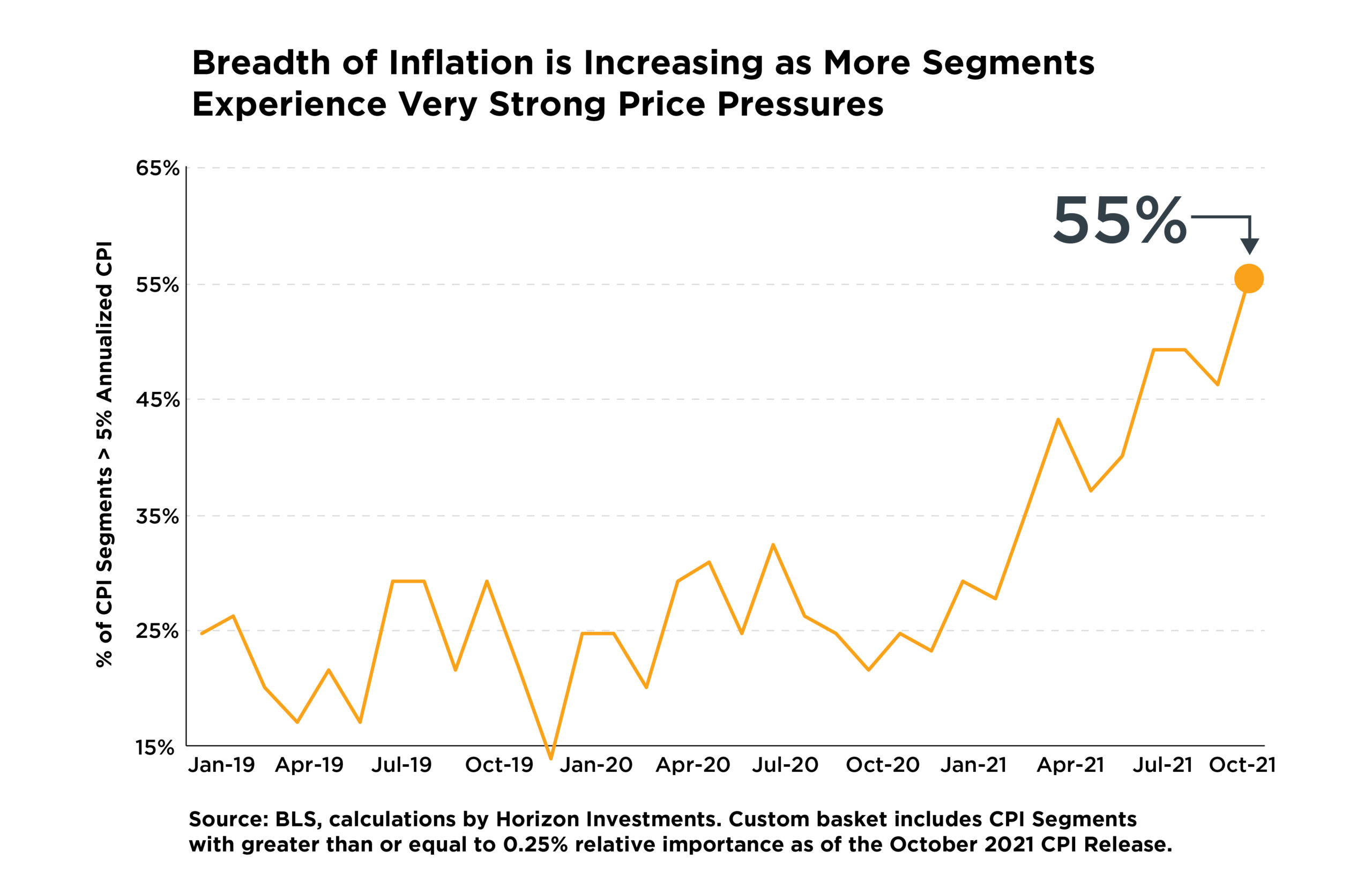

In October, the prices for more than half of the items in the Consumer Price Index (CPI) were rising at a rate of at least 5% per year, according to Horizon Investments’ calculations using Bureau of Labor Statistics data. A year ago, the same stat applied to only a quarter of the CPI’s items.

Among the wide range of things that got more expensive last month: gasoline, natural gas, electricity, used cars, full-service meals, flour, cereal, rice, beef, fish, pork, tools, and hardware. The rapid spread of fast-rising prices is spurring calls for politicians to find ways to reduce the pain.

Focusing just on the price increases, however, misses the larger inflation forces that are at play, forces that could still make this a temporary, supply-chain driven spike in the cost of living.

Worker productivity and technological innovation are two important deflationary forces. They played a major role in the tame inflation environment of the pre-pandemic years. Horizon Investments’ view is that if someone is going to argue that we’re going to experience rampant, long-lasting inflation, then they’re saying that the productivity and innovation engines in the U.S. are broken. We don’t agree with that. See our Q3 Focus, “2022 Outlook,” for articles on inflation and the economy that describe why we believe that this bout of inflation shall pass once supply chains are repaired.

Third quarter corporate earnings reports suggest productivity and innovation are still strong forces. Operating profit margins rose to 15% for the companies in the S&P 500 Index, according to Bloomberg data. Corporations have generally stayed ahead of price pressures through efficiency gains, labor-saving technology, product substitutions or price hikes for their own products.

Fatter profit margins are a testament to the flexibility, adaptability, and speed of change that can take place in modern companies, and helps explain why equities haven’t tumbled amid rising inflation.

Still, our view doesn’t diminish the potential pain inflation can cause retirees and those saving for retirement and other long-term goals. Higher prices are a direct threat as inflation-adjusted investment returns could buy less in the future. Inflation can be particularly difficult for investments in fixed income, especially for those whose returns are currently negative when taking the cost of living into account.

In today’s unusual period of time, Horizon Investments believes in the importance of adding as much equity exposure as someone is comfortable with for reaching their long-term financial goals. That includes people nearing or in retirement. They may need their nest egg to support them for a long time, potentially 25 years or more, with inflation being a key detail in determining their standard of living.

To put it simply: we believe equities currently offer more opportunities for inflation-beating returns than fixed income. And the current cost of living increases exemplify why our Real Spend® retirement income strategies tilt in favor of stocks rather than bonds in the quest to overcome longevity risk.

Further reading:

Baby Boomer Retirees May Be Crushed by Zero

3Q Focus Magazine: Outlook 2022, The Next Unprecedented Year

The Biggest Retirement Fear? Outliving My Money

Are Glide Path Strategies Still a Good Option for Retirement?

If Inflation Returns, Bond’s Diversification Power May Disappear

Essentially Nothing. That’s How Much Bonds May Return Over Next Five Years