Inflation is a difficult thing to define, in part because each person’s buying habits affect their perception of it. If you’re not buying lumber, then the meteoric rise in price may not be apparent to you other than in news stories.

For the purposes of this blog post, we need a common inflation barometer, and Horizon Investments’ goals-based perspective focuses on the Consumer Price Index (CPI). The index affects markets and is the topic of news stories that influence the public’s view. Will CPI readings get hotter? Yes, if you’re measuring this year’s prices against 2020’s depressed readings when the economy was shut down. Economists talk about that as a “base effect,” meaning part of the expected CPI surge reflects the fact that last year was so weak.

Inflation headlines are coming

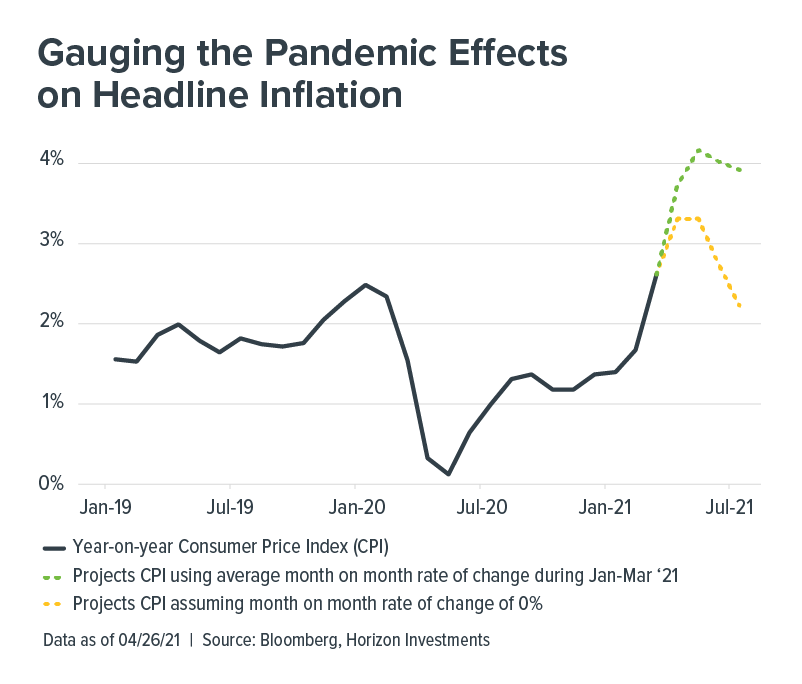

The chart above illustrates Horizon’s projection for initially hot inflation readings, and then a cooling off. The green line uses this year’s average month-to-month increase in CPI and applies that to the next few months. The hypothetical scenario produces a 4%+ year-on-year inflation rate at the peak.

Even a benign scenario – assuming no month-to-month acceleration in CPI (the yellow line) – has headline inflation printing over 3%, which would be a nine-year high.

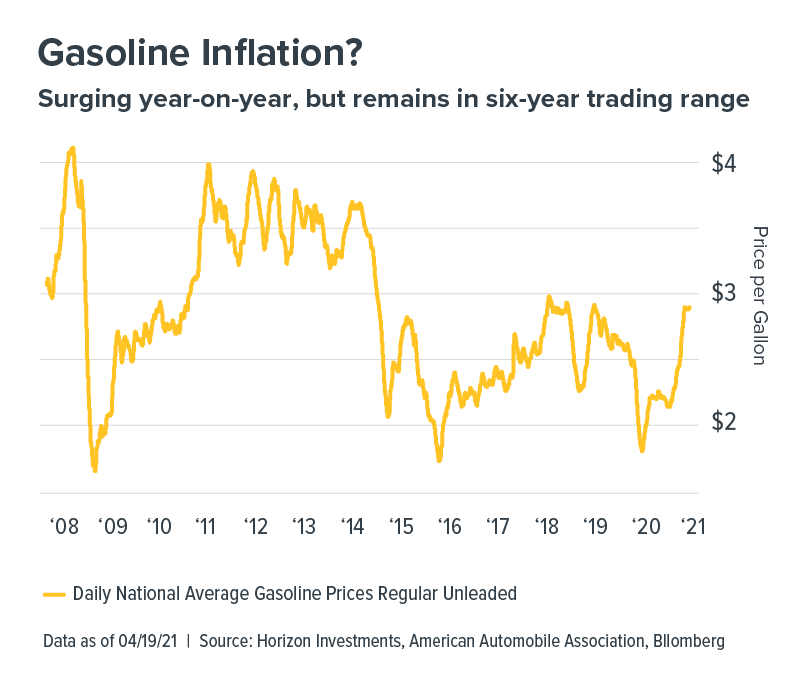

But the important point is that once we get past April, May and June, the year-on-year surge fades, because by that point in 2020 inflation was rebounding, and so the “base effect” on the data also fades. An everyday example of the phenomenon comes from the gas station.

Pump prices are 22% higher compared to March last year!! And the national average price is nearing $3 a gallon when it was closer to $2 just a few weeks ago!! True. But remember that recency bias colors our perception. What’s forgotten is that last year’s price was unusually low, and in the months ahead the year-on-year increase will be smaller than it was in March. We also should remember that current gasoline prices are normal compared to the last few years. (FYI, there’s no supply/demand imbalance in gasoline like there is in lumber. Gasoline days of supply is currently 26, according to Energy Department data as of April 21, inline with the average of 24 days’ supply for the 20 years stretching from January 2000 to March 2020.)

CPI measures hundreds of things

When measuring inflation, gasoline is just one of hundreds of items tracked by CPI. The year-over-year surge in pump prices was offset to some degree by items which were tumbling in price with people at home, such as clothing and auto insurance. It’s important to remember that whatever headline is driving the inflation-to-the-moon narrative, it’s usually just a small part of what’s being measured. CPI is constructed as an average of what people spend their money on. And its most-important items, shelter and food, are given the most weight, as they affect everyone.

Whether it will happen depends on worker output, or productivity. If higher wages and benefits result in greater output, that should put no upward pressure on broad inflation measures. There’s evidence that may happen. If work-from-home becomes ingrained, that could lead to a 5% boost in U.S. productivity, Bloomberg News reports citing a study co-authored by researchers at Stanford University, the University of Chicago Booth School of Business and the Instituto Tecnológico Autónomo de México that polled over 30,000 U.S. workers.1 The study found that 20% of full workdays will be from home after the pandemic, compared with just 5% before it began.

The ECI data isn’t as sexy as lumber prices or GameStop’s stock – however, it’s the crux of the inflation question and it will play a prominent role in the Federal Reserve’s future discussions of whether inflation is getting too hot and interest rate hikes are needed.

Goals-Based plans & inflation

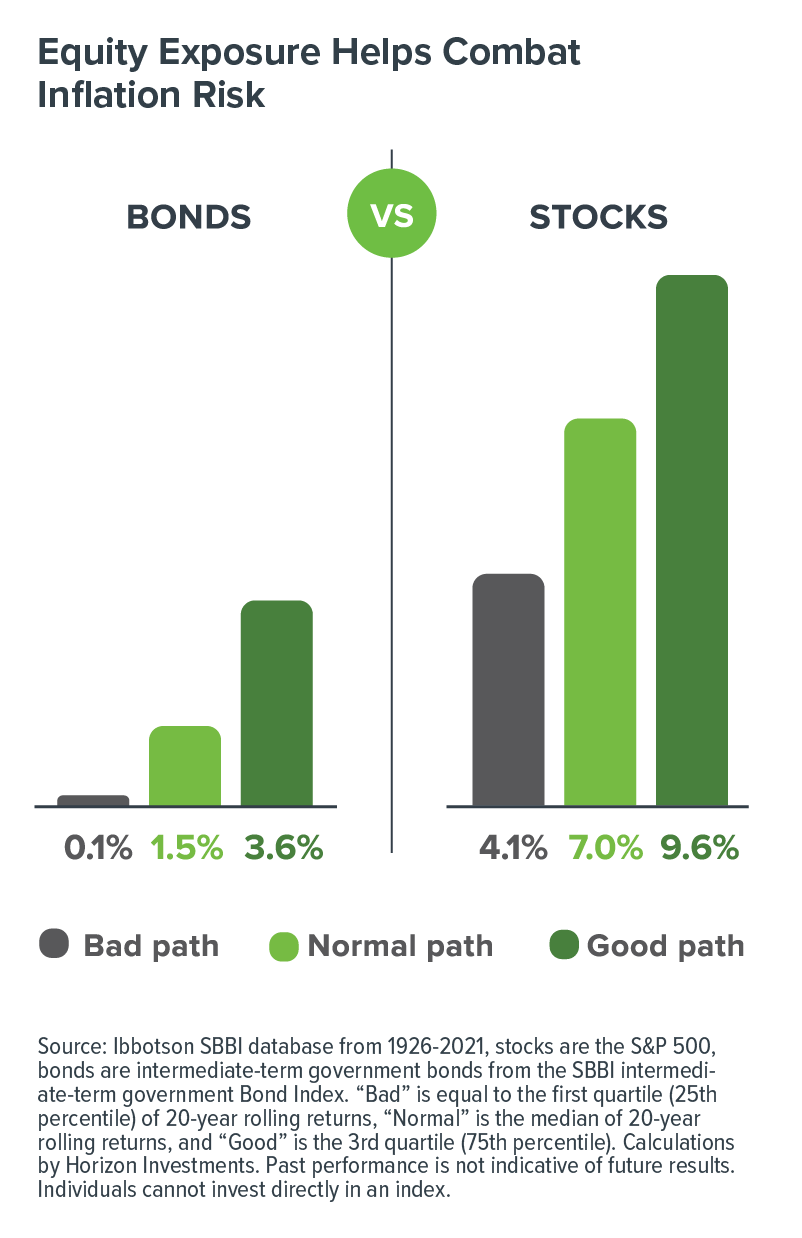

For goals-based investors in the Gain and Protect stages, we believe the inflation conversation is largely a distraction. Wages would likely respond to an increase in inflation, and over long periods, stocks have historically outpaced the rising cost of living.

In Horizon’s research on retirement funding shows that even during a “bad” 20-year rolling return period for stocks, inflation-adjusted returns outpace the best periods for a broad bond-market investment.

Inflation risk is a more urgent issue for newly retired people, who face a 20- to 30-year retirement. Today’s low bond yields, we believe, are unlikely to beat the current rate of inflation, and bond returns will be hamstrung if inflation accelerates (see our Q1 Focus report “Crushed by Zero”).

Horizon created its Real Spend® suite of solutions with the goal of mitigating retirement inflation risks better than traditional portfolio construction which calls for more bond exposure as people age.

Our flexible investment strategy – embracing bond alternatives alongside traditional fixed-income – allows us to adapt should the Federal Reserve decide to combat inflation by raising interest rates. In addition, Real Spend® portfolios are designed to tilt to equities because we believe in their long-term, inflation-beating power.

We believe the combination of these components within a single strategy gives retirees the best probability of ensuring people don’t outlive their money. In an environment where inflation risks are higher than they’ve been in years, Horizon’s Real Spend® strategies offer a solution rooted in research, yet practical in application.

1 “Work From Home to Lift Productivity by 5% in Post-Pandemic U.S.,” Bloomberg News, 4/22/21