Fuhgettaboutit

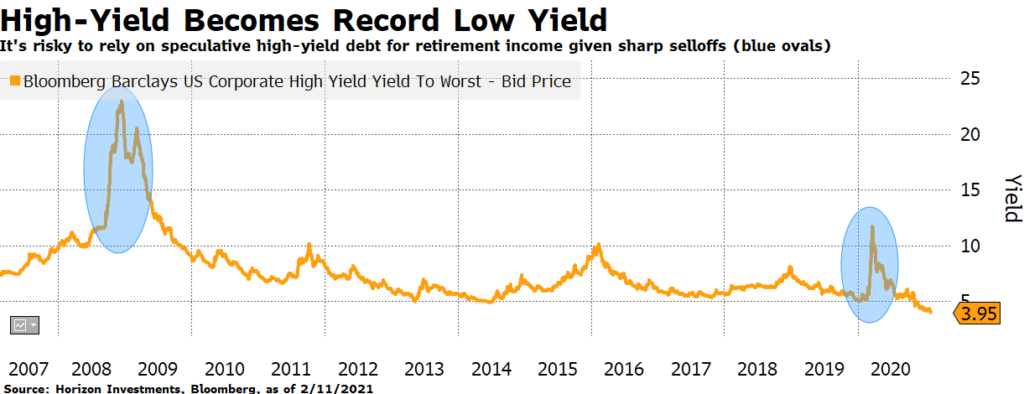

Here’s another knock against putting all of your retirement-income eggs in the bond market basket. This week is ushering in record low yields of less than 4% for high-yield corporate debt. While that yield is rich compared to the 10-year Treasury, using speculative junk bonds to provide the income investors expect from their fixed-income allocation can be risky when the good times end (see blue ovals below). For example, high-yield, as proxied by the Bloomberg Barclays US Corporate High Yield Index, lost 12.7% in total return in Q1 of 2020 as the pandemic hit. Today, yields are about 1.25% lower than where they started 2020.

At Horizon, we believe the Fed’s accommodative stance, coupled with the coming economic recovery, will keep high-yield valuations elevated. We own high-yield debt in our fixed-income portfolios, but we aren’t adding to that allocation at these yield levels. Rather, we currently prefer to express our positive stance on asset markets through a diversified set of alternative fixed-income instruments, including preferred equities, convertible bonds, bank loans and emerging market debt.

Red Ink

Elsewhere in the bond market, losses are already hitting longer-dated corporate debt. Bloomberg reports that corporate bonds with at least 10 years left to maturity have produced losses of around 3.2% so far in 2021, the worst start to any year since 2018. Corporate bonds are being hurt by the economic reflation trade and the duration risk that comes with holding long-term debt in a potentially inflationary environment.

And remember the Big Number report Horizon published on December 17 pointing out that investment grade corporate bonds now carry a negative yield when you factor in expected inflation? Since then, the inflation-adjusted negative yield has worsened to -33 basis points, as of February 11.

Inflation, however, is still a no show; at least that’s good news for bonds. The Consumer Price Index came in below economist expectations and core prices remain well below the Federal Reserve’s 2% target.

And Federal Reserve chairman Jay Powell’s speech indicated – once again – he’s years away from raising rates, which can keep a bid in bonds despite the potential risks posed by low yields, faster economic growth and inflation.

Shocking earnings season news keeps rolling in!

S&P 500 Q4 earnings and sales are now on pace to grow year-on-year, defying analysts’ forecast for a drop. The magnitude of the surprise is larger than the typical lowering-of-the-bar that goes on ahead of earnings season. Bloomberg Intelligence sees Q4 EPS growing 3.6% versus the analysts’ pre-season forecast for a drop of 8.8%. In our opinion, this will likely cause analysts to raise their 2021 earnings forecasts.

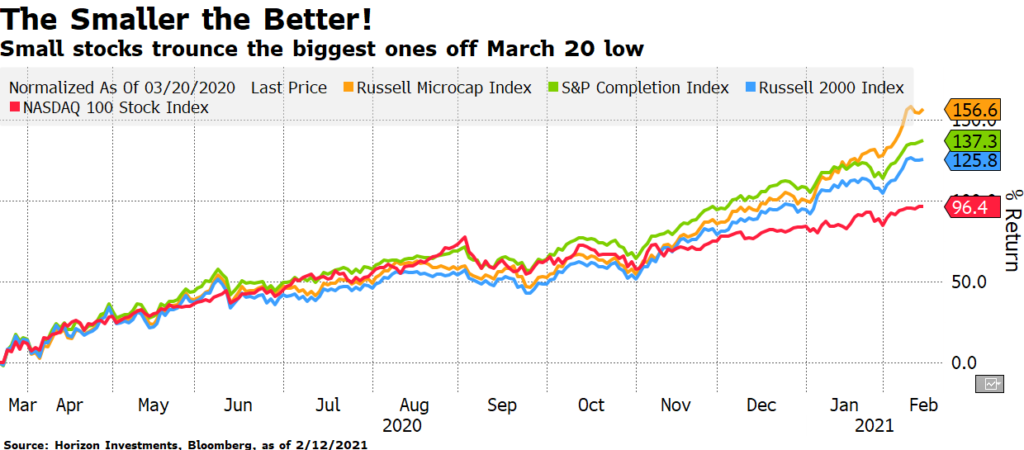

Such good earnings news is helping propel U.S. stocks to record highs, along with the prospect of trillions more in government stimulus and expanding vaccinations. The breadth of the advance has not been concentrated in large-cap tech stocks. The small companies are in fact the biggest gainers not only this week, but also off of last year’s lows. Horizon Investments recently added to its overweight on small-cap stocks versus large-caps given our optimistic outlook for the back half of 2021. Smaller companies are generally not a large allocation for many investors given the dominance of mega-cap companies in recent years. Horizon’s flexible, active approach allows us to take advantage of new trends as markets change.

Also making all-time highs are the S&P 500 equal weight index (another sign of a broad rally) , S&P 500 cumulative breadth and the MSCI Emerging Markets index.

Related stories:

Do Bonds Really Offset Stock Market Declines?

If Inflation Returns, Bond’s Diversification Power May Disappear

Essentially Nothing. That’s How Much Bonds May Return Over Next Five Years

Only Two Words Matter to Markets: Stimulus Spending

PIIGS Fly and Other Stories of Investors Reaching for Risky Bets

Momentum’s No Longer the Stock Market King, Vaccine Will Raise New Leadership

It’s Getting Harder to Fund Retirement Using Bonds

7.9 Trillion Reasons Not to Fight the Fed, ECB, BOJ or BOE

This commentary is written by Horizon Investments’ asset management team. For additional commentary and media interviews, contact Chief Investment Officer Scott Ladner at 704-919-3602 or sladner@horizoninvestments.com.

To download a copy of this commentary and the chart of the week, click the button below.

To discuss how we can empower you please contact us at 866.371.2399 ext. 202 or info@horizoninvestments.com.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments. It is not possible to invest directly in an index.

Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent.

Other disclosure information is available at www.horizoninvestments.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2021 Horizon Investments LLC

Insights

Disappearing Junk Bond Yields

Share:

Fuhgettaboutit

Here’s another knock against putting all of your retirement-income eggs in the bond market basket. This week is ushering in record low yields of less than 4% for high-yield corporate debt. While that yield is rich compared to the 10-year Treasury, using speculative junk bonds to provide the income investors expect from their fixed-income allocation can be risky when the good times end (see blue ovals below). For example, high-yield, as proxied by the Bloomberg Barclays US Corporate High Yield Index, lost 12.7% in total return in Q1 of 2020 as the pandemic hit. Today, yields are about 1.25% lower than where they started 2020.

At Horizon, we believe the Fed’s accommodative stance, coupled with the coming economic recovery, will keep high-yield valuations elevated. We own high-yield debt in our fixed-income portfolios, but we aren’t adding to that allocation at these yield levels. Rather, we currently prefer to express our positive stance on asset markets through a diversified set of alternative fixed-income instruments, including preferred equities, convertible bonds, bank loans and emerging market debt.

Red Ink

Elsewhere in the bond market, losses are already hitting longer-dated corporate debt. Bloomberg reports that corporate bonds with at least 10 years left to maturity have produced losses of around 3.2% so far in 2021, the worst start to any year since 2018. Corporate bonds are being hurt by the economic reflation trade and the duration risk that comes with holding long-term debt in a potentially inflationary environment.

And remember the Big Number report Horizon published on December 17 pointing out that investment grade corporate bonds now carry a negative yield when you factor in expected inflation? Since then, the inflation-adjusted negative yield has worsened to -33 basis points, as of February 11.

Inflation, however, is still a no show; at least that’s good news for bonds. The Consumer Price Index came in below economist expectations and core prices remain well below the Federal Reserve’s 2% target.

And Federal Reserve chairman Jay Powell’s speech indicated – once again – he’s years away from raising rates, which can keep a bid in bonds despite the potential risks posed by low yields, faster economic growth and inflation.

Shocking earnings season news keeps rolling in!

S&P 500 Q4 earnings and sales are now on pace to grow year-on-year, defying analysts’ forecast for a drop. The magnitude of the surprise is larger than the typical lowering-of-the-bar that goes on ahead of earnings season. Bloomberg Intelligence sees Q4 EPS growing 3.6% versus the analysts’ pre-season forecast for a drop of 8.8%. In our opinion, this will likely cause analysts to raise their 2021 earnings forecasts.

Such good earnings news is helping propel U.S. stocks to record highs, along with the prospect of trillions more in government stimulus and expanding vaccinations. The breadth of the advance has not been concentrated in large-cap tech stocks. The small companies are in fact the biggest gainers not only this week, but also off of last year’s lows. Horizon Investments recently added to its overweight on small-cap stocks versus large-caps given our optimistic outlook for the back half of 2021. Smaller companies are generally not a large allocation for many investors given the dominance of mega-cap companies in recent years. Horizon’s flexible, active approach allows us to take advantage of new trends as markets change.

Also making all-time highs are the S&P 500 equal weight index (another sign of a broad rally) , S&P 500 cumulative breadth and the MSCI Emerging Markets index.

Related stories:

Do Bonds Really Offset Stock Market Declines?

If Inflation Returns, Bond’s Diversification Power May Disappear

Essentially Nothing. That’s How Much Bonds May Return Over Next Five Years

Only Two Words Matter to Markets: Stimulus Spending

PIIGS Fly and Other Stories of Investors Reaching for Risky Bets

Momentum’s No Longer the Stock Market King, Vaccine Will Raise New Leadership

It’s Getting Harder to Fund Retirement Using Bonds

7.9 Trillion Reasons Not to Fight the Fed, ECB, BOJ or BOE

This commentary is written by Horizon Investments’ asset management team. For additional commentary and media interviews, contact Chief Investment Officer Scott Ladner at 704-919-3602 or sladner@horizoninvestments.com.

To download a copy of this commentary and the chart of the week, click the button below.

To discuss how we can empower you please contact us at 866.371.2399 ext. 202 or info@horizoninvestments.com.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments. It is not possible to invest directly in an index.

Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent.

Other disclosure information is available at www.horizoninvestments.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2021 Horizon Investments LLC

Follow us on: