Short-Term Market Volatility

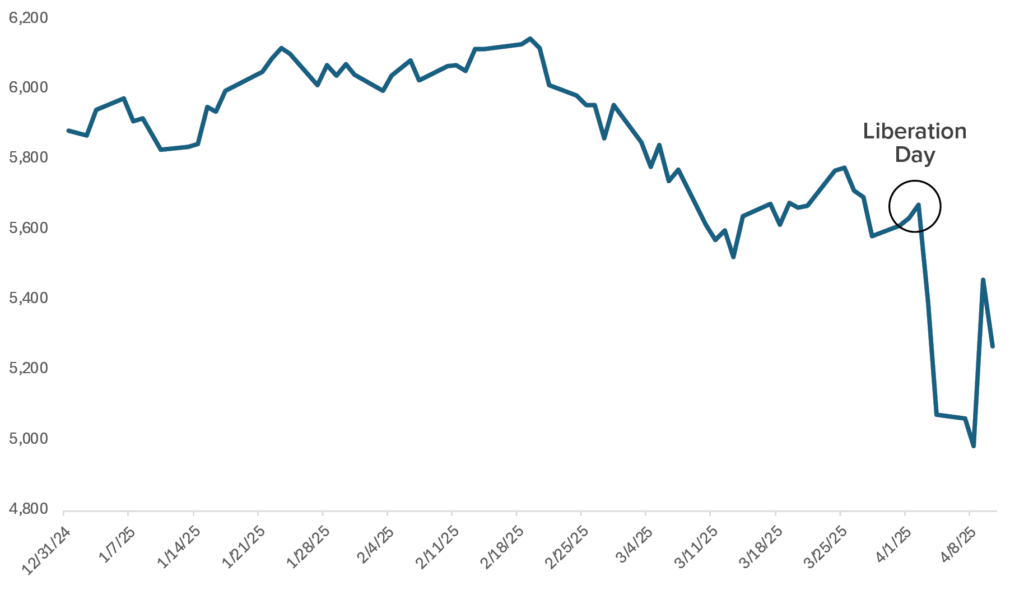

Market volatility over the past week has been nothing short of historic. The two-day loss in the S&P 500 in the wake of the Liberation Day announcement was -10.5%, the fifth largest since World War II. Likewise, the 9.5% one-day gain in the S&P 500 after President Trump delayed the imposition of some tariffs on April 9 was only exceeded during the 2008 Global Financial Crisis and the Great Depression. Stocks have since unwound some of that move, but the volatility remains, nonetheless.

S&P 500 Year-to-Date Performance

Source: Bloomberg, calculations by Horizon Investments, data as of 04/10/25. The S&P 500 or Standard & Poor’s 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. Past performance is not indicative of future results. It is not possible to invest directly in an index.

Amid all the noise and volatility over the past few weeks, one of our key takeaways is the performance of long-term U.S. Treasuries and the dollar relative to other periods of major market stress. Given the U.S.-centric nature of the recent developments, market participants have fled dollar-based assets, leading to weakness in the dollar and lower prices for U.S. Treasuries. Additionally, the material underperformance of domestic equities, especially technology, relative to international stocks has called into question the idea of “U.S. exceptionalism” and the premium valuation multiples domestic stocks have commanded. International equity diversification was rewarded in the first quarter, and seeing it continue in a major risk-off period may be a sign of a sea change in the market trends in place for much of the past 15 years.

We think the key market takeaway from the past week is best understood by examining the performance of global stocks (especially U.S. tech), U.S. long-term interest rates, and the U.S. Dollar relative to our major trading partners. Specifically:

- U.S. equities underperforming international equities

- U.S. long term yields rose significantly, pushing Treasury prices lower

- A weaker U.S. Dollar

Long-Term Uncertainty

Stepping back from the market activity, massive tariffs remain on China, as well as an across-the-board 10% tariff on all our trading partners. Trump’s actions on April 9 dramatically increased the tariffs on China but put a three-month pause on the reciprocal tariffs on our other trading partners announced last week. As we’ve noted, U.S. trade is highly concentrated with Mexico, China, and Canada – making these three nations the most critical players in trade negotiations. While the broader situation remains far from resolved, this concentration does provide the opportunity to narrow the focus to the conversations likely to have the greatest economic impact.

It is important to remember that this is a man-made economic and market situation and it can be UN-man-made as well. As we saw on April 9 with the 90-day pause announcement, the current market environment can change with a single headline. Reporting indicates that it wasn’t necessarily the stock market volatility, but rather the increase in long term yields, that got the attention of economic advisors in the White House. Before Trump’s pause announcement, the 30-year Treasury yield climbed over 50 basis points since Liberation Day, and the dollar had notably weakened – both clear signals of rising threats to U.S. financial stability. While market functioning has improved over the past two business days, uncertainty remains high. This lingering uncertainty will likely continue to weigh on valuations and market prices, making a near-term recovery to new highs unlikely. And while the most immediate growth-negative risks around trade may have eased, the probability of a recession has not meaningfully declined.

Concluding Thoughts

History reminds us that in the days following deep dives like what we’ve seen over the last week, markets have tended to rebound quickly. We anticipate that consumers and businesses will maintain a hunkered-down position as we continue to wait and see how the short- and long-term implications of Liberation Day play out amid ongoing negotiations. First quarter earning season is also underway and will serve as an additional temperature check from a corporate health standpoint.

At the same time, ongoing uncertainty around tariff policy will likely continue to fuel volatility in the near term. This contrast is an important reminder of the message we shared in our Liberation Day publication: It’s critical to stay the course during periods of market disruption.

These three reminders hold:

- Diversification is essential: Spreading investments across sectors, industries, and regions can help reduce concentration risk and improve portfolio resilience.

- Stay invested and avoid emotional decision-making: Market volatility can wreak havoc on investment portfolios and investor nerves. And when emotions run high, decision-making can suffer. Reminding investors not to make investment decisions that can derail a long-term financial plan is critical.

- Consider risk mitigation strategies to weather volatility: Investors with a higher aversion to investment loss may be tempted to move assets to the sidelines and weather out the storm. While each scenario is different, disciplined risk mitigation strategies can help preserve wealth, reduce anxiety, and help keep portfolios on track.