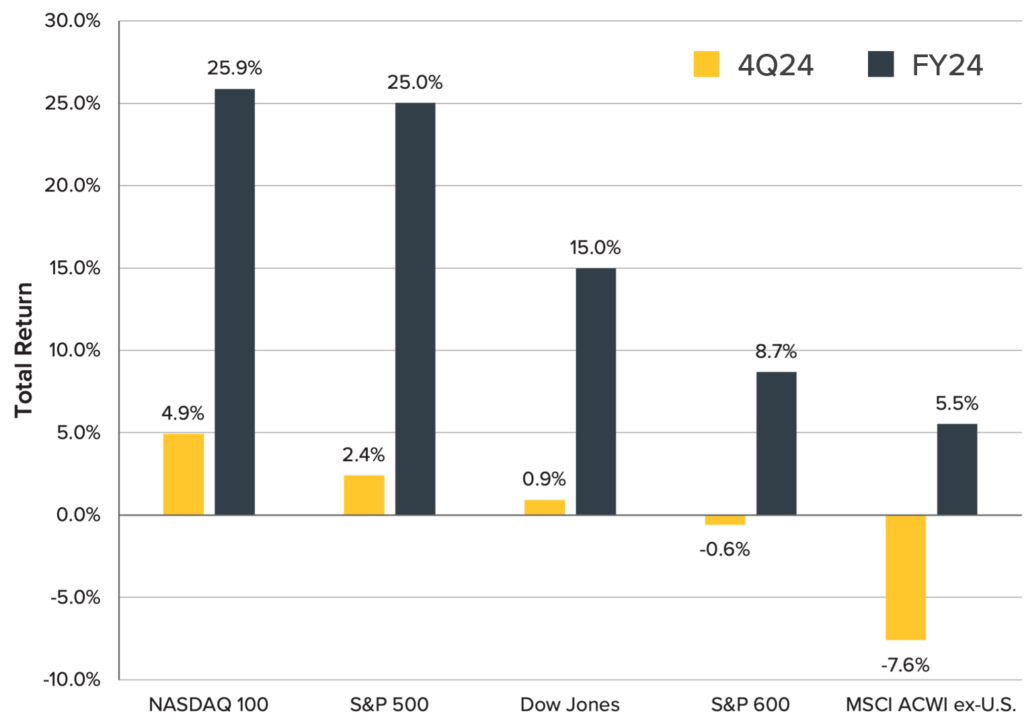

Exhibit 1: Major Stock Market Indices Returns (Q4 2024)

Source: Bloomberg, calculations by Horizon Investments, data as of 12/31/2024. Indices are unmanaged and do not have fees or expense charges, both of which would lower returns. It is not possible to invest directly in an unmanaged index.

As 2025 begins, a variety of factors are set to play a role in how the financial markets behave going forward. Ultimately, however, there are three key pillars that we believe will drive opportunities and risks in the coming year:

1. The Economy: Rising Expectations, With Implications for Small-Caps

After several years of pessimism from consumers about the state of the economy, expectations for business conditions over the next six months rose during much of the fourth quarter as consumers expressed an overall sense of optimism about the road ahead.

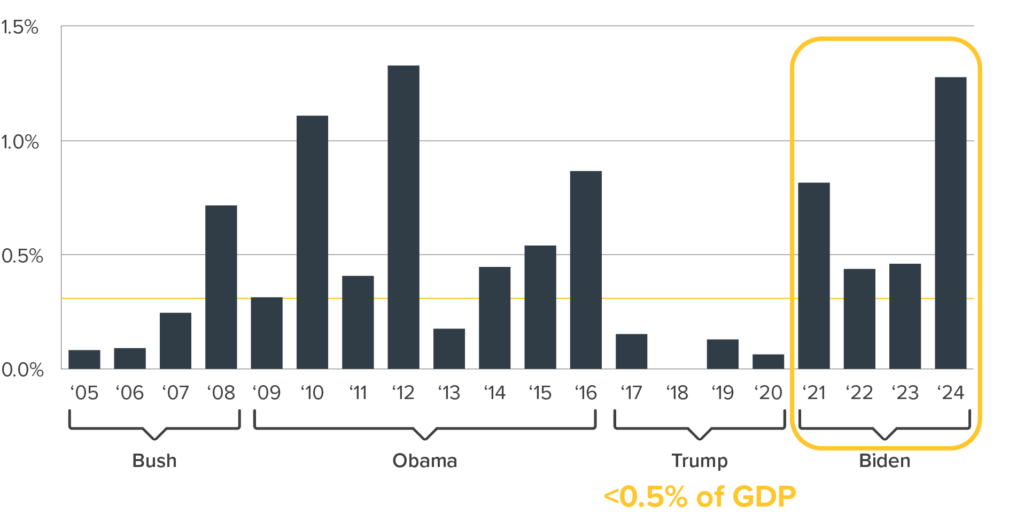

That rising optimism was sparked by the lower corporate tax rates and lower regulatory costs expected to occur as Republicans take over leadership of both Congress and the White House in January. Note, for example, that the total cost of regulations during Trump’s first Presidency was significantly lower than it was under both the Obama and Biden administrations (see Exhibit 2).

Exhibit 2: Total Cost of Regulations by Year (%GDP)

Source: Piper Sandler, 11/20/2024. Information obtained from third-party sources is believed to be reliable but has not been vetted by the firm or its personnel.

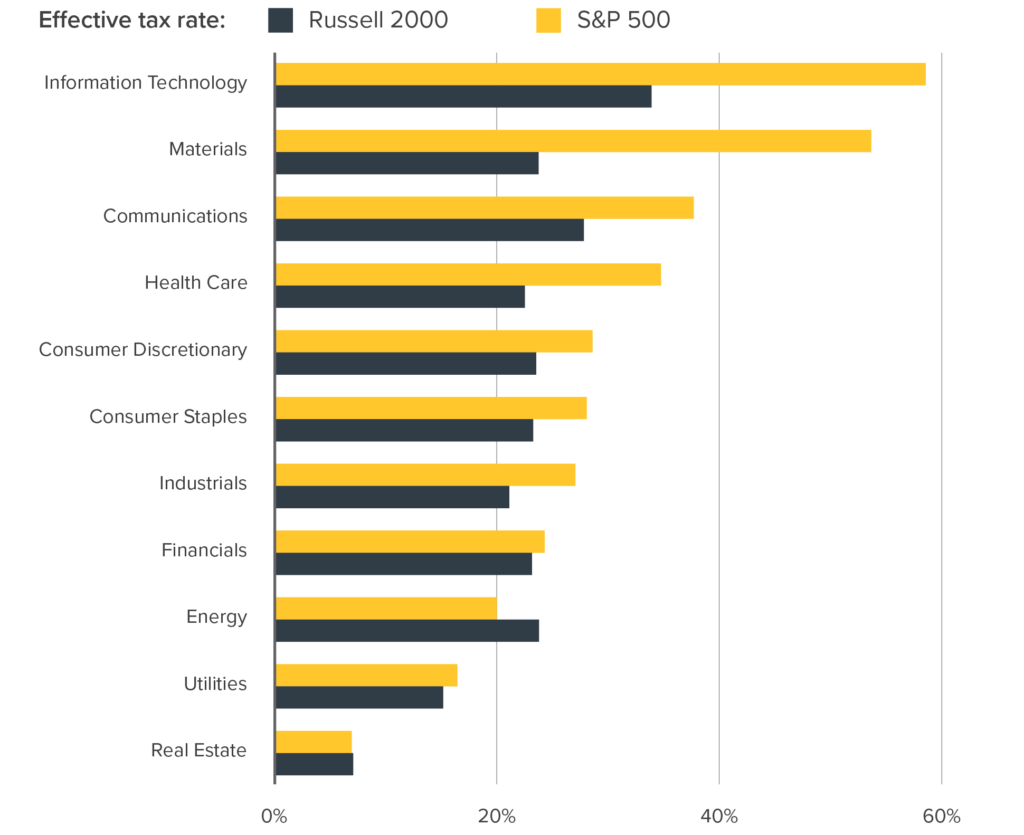

In particular, small and mid-sized companies may benefit substantially from lower taxes and regulatory expenses. Such costs have an outsized impact on these businesses. For example:

- Regulatory costs (as a percentage of total labor costs) are highest for companies with fewer than 500 employees.

- The effective corporate tax rate is higher for smaller firms than for larger ones in nearly every market sector (see Exhibit 3).

Exhibit 3: Corporate Tax Burden – Small Companies vs. Large Companies

Source: RBC, 11/12/2024. Information obtained from third-party sources is believed to be reliable but has not been vetted by the firm or its personnel.

2. Consumers: Robust Financial Strength Still in Place

U.S. consumers continue to maintain healthy personal balance sheets—benefiting from a resilient labor market, rising incomes, manageable debt levels and growing net worths. For example:

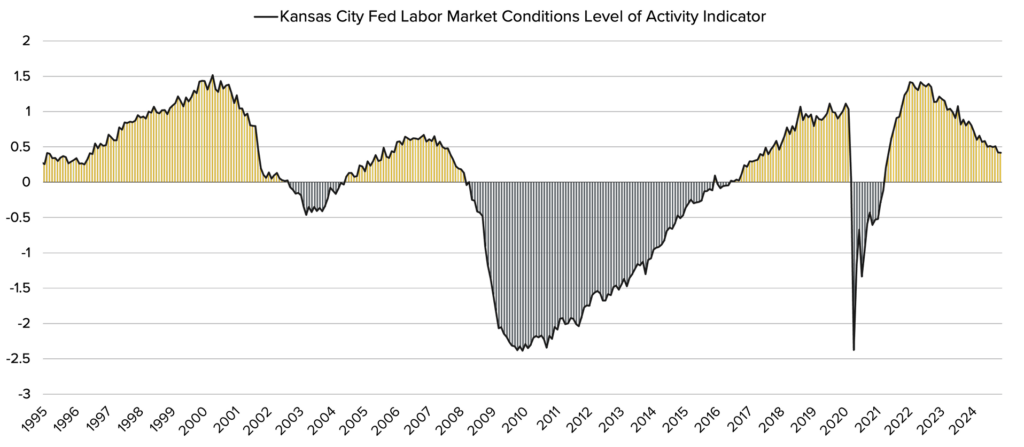

- Resilient jobs market: While the labor market has cooled from its rapid expansion in 2022 and 2023, it is far from weak. As seen in Exhibit 4, a broad measure of labor market conditions is now at roughly the same level it was in 2017—consistent with a more stable economy.

Exhibit 4: Labor Market Conditions

Source: Bloomberg, calculations by Horizon Investments, 12/18/2024. Information obtained from third-party sources is believed to be reliable but has not been vetted by the firm or its personnel.

- Manageable debt levels: Consumers’ rising debt levels have created a lot of attention. But the fact is, consumers’ credit card debt and overall aggregate debt levels relative to their disposable incomes are at or near historic lows. In short, consumers overall can service their debt.

- Rising incomes: Despite a sense that wages haven’t kept pace with prices, a recent study from Brookings shows that total compensation has exceeded inflation over the 2019-2024 period for workers.

- Growing net worth: Overall household net worth is up meaningfully since the end of 2019, and has more than recovered from its brief dip in 2022. It has also exceeded the rate of inflation over that period. A major contributing factor has been rising home prices in recent years, which has created a stunning $35 trillion in estimated home equity today—an amount that is larger than the U.S.’s entire annual gross domestic product. The resulting wealth effect is motivating more homeowners to leverage some of that net worth. Consider, for example, the sharp rise in the number of home equity lines of credit since 2021 (see Exhibit 5).

Exhibit 5: Total Home Equity Lines of Credit

Source: Federal Reserve Economic Data, 12/12/2024. Information obtained from third-party sources is believed to be reliable but has not been vetted by the firm or its personnel.

3. Financial Markets: Expect Some Turbulence

Several factors indicate the stock market is well positioned to build on its gains in 2024, including:

- Fundamentals: Earnings growth estimates for 2025 are healthy for technology companies in the S&P 500 as well as non-tech firms in the index. However, the gap between tech and non-tech companies’ earnings growth estimates is closing, according to a recent UBS report. That suggests to us that stock gains may broaden out in the coming year as investors look beyond tech and large-cap to other market areas.

- Momentum: Early in 2024, we pointed out that new stock market highs tend to be followed by more new highs rather than by downturns. With the S&P 500 up 25% for the year, there’s a strong probability of further gains in 2025.

That said, some areas of uncertainty cloud the forecast for equity market performance during the coming year.

Chief among them are signs that the fight to subdue high inflation may not be over, due to potential new policies from the Trump administration and surprising strength from the economy. Although inflation moderated enough to allow the Fed to cut interest rates three times in 2024, the Fed noted that it may take longer than expected for inflation to hit the Fed’s 2% target. As seen in Exhibit 6, the Fed’s inflation outlook shifted sharply from September to December—with many more Fed members now seeing an upside risk of inflation than they did three months ago.

Exhibit 6: Fed Sees Rising Risk of Inflation Pressures

Source: Federal Reserve Economic Data, 12/18/2024. Information obtained from third-party sources is believed to be reliable but has not been vetted by the firm or its personnel.

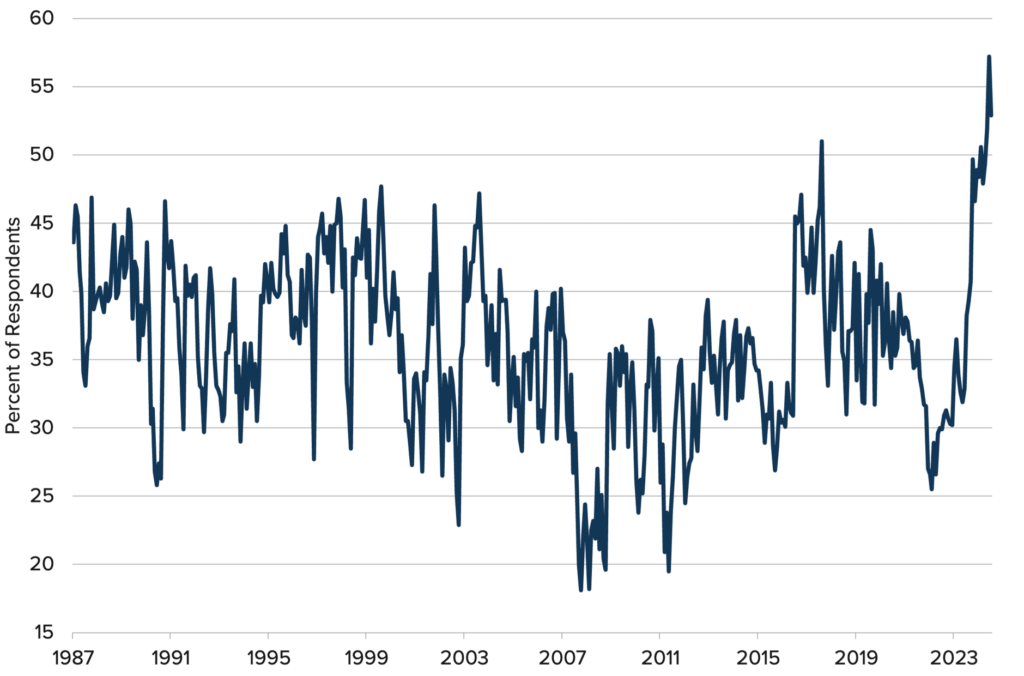

In addition, investor sentiment is hitting a bullish level that may indicate overconfidence in the market’s ability to keep rising. The percentage of consumers expecting stocks to rise has soared to its highest point on record (see Exhibit 7) —and according to a Bank of America Global Fund Manager Survey, the overall stocks versus cash position in portfolios is at a ratio that, based on history, may signal future volatility.

Exhibit 7: Is Investor Sentiment Too Bullish?

Source: Bloomberg Opinion, 12/18/2024. Information obtained from third-party sources is believed to be reliable but has not been vetted by the firm or its personnel.

The upshot: While our 2025 outlook remains positive and constructive, turbulence risk appears to be higher than during much of 2024.