The newest twist on snarled supply chains and inflation? A global energy crunch.

Intense competition is causing soaring prices for limited inventories of natural gas, oil, and coal as green energy policies reduce reliance on fossil fuels, while the fickle weather reduces renewable energy output worldwide. The unexpected pop in prices may hit global GDP growth and potentially sustain a higher rate of inflation, pressuring central bankers around the world to raise interest rates.

The combination of soaring prices, inflation pressures, and the hit to economic growth has some people raising the specter of a replay of the 1970’s stagflationary environment, when there was a combination of slow GDP growth and sticky inflation.

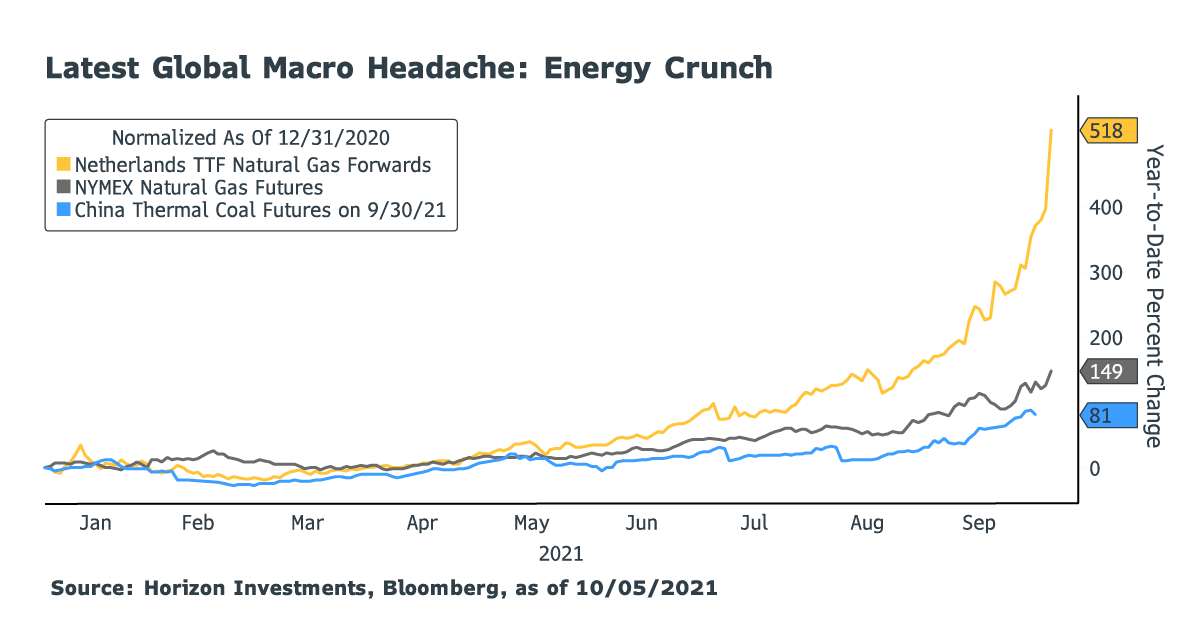

Many factors are hitting at once to cause the parabolic move in some energy prices, including lower-than-normal stockpiles of fuels, a drop in renewable energy output, Russian pipelines delivering less gas than what’s needed in Europe, and a drought in China that’s hurting hydro-electric output as electricity demand soared with a reopening economy.

Lastly, OPEC decided this week to stick with its measured boost of crude oil output, dashing hopes it would pump more.

The macroeconomic implications from the current energy spike could be wide-ranging:

- GDP growth in Europe and China may be reduced as corporate and consumer spending is re-routed to utility bills rather than consumption of goods and services

- European food costs may rise as energy-intensive Dutch greenhouses, which supply many fresh foods across the continent, reduce production

- Supply chain bottlenecks may not get resolved as Chinese factories reduce output as part of government orders to reduce power consumption

- Corporate profit forecasts may need to be adjusted as energy prices squeeze margins and sales tumble as customers divert money to paying their utility bills

However, the comparison to the1970s environment ignores crucial differences today compared to 50 years ago:

- The energy intensity of GDP is half of what it was in the 1970s

- It currently takes 0.43 barrel of oil to produce $1,000 of global GDP versus nearly 1.0 barrel of oil to produce the same amount of GDP in 1973, according to Columbia University’s Center on Global Energy Policy1

- OPEC remains a powerful force in crude oil markets with 40% market share, down from the 1970s when it held 56%2 of the market and instituted an embargo on sales to the U.S. during a military conflict

- U.S. frackers (a technological breakthrough that wasn’t available in the 1970s) could rapidly increase production, though they currently have been slow to do so amid investor demand for fiscal discipline

- The U.S. is now an exporter of oil versus being a major importer 50 years ago

Horizon Investments continues to believe that the supply/demand mismatches that are leading to higher prices in many products will be ironed out. And when that occurs, inflationary pressures could ease. We saw this with car and truck rental prices which sank 7% month on month in the August Consumer Price Index (CPI) report as more rentals were available. Compare that to April’s CPI report when rental prices soared by 15% as demand outstripped the number of available vehicles for rent.

(Read Horizon’s Redefining Risk paper to understand our goals-based investing philosophy)

That said, Horizon’s goals-based investment management process is built to be flexible and dynamic – rather than dogmatic. As market leadership and macroeconomic conditions evolve, our Gain stage investing strategies aim to adapt to those changes to help deliver the risk-adjusted returns investors are seeking to reach their long-term financial goals. That same flexibility is also how Horizon constructs its strategies for the Protect and Spend stages.